Are your liquid assets illiquid?

Hazards and rewards of investing in hard-to-trade assets in the current economic environment

Welcome to in the mood for wine — a weekly newsletter on wine for the next gen of wine lovers and investors. Please hit the heart button if you like today’s newsletter and reply with any feedback.

TL;DR

We analyse the liquidity of wine investments along three axis: bid-ask spread, investment horizon and current economic environment.

Liquidity ⬇️ as bid-ask spread ⬆️, investment time horizon ⬆️ and/or at times of monetary (and fiscal) tightening.

Liquidity isn’t static: it varies over time and across assets.

The topic of this article came to me following a conversation with one of my followers.

He mentioned that he was thinking of buying Carruades 2021 (Château Lafite Rothschild second wine) because “it’s the cheapest wine currently available […] and Liv-ex secondary bids suggest that it had already appreciated +23.2% from release price”.

That is, of course, a very strong buy signal from the secondary market. To put it into context, investing in the stock market (say, the S&P 500) would yield a total return of +20 to 30% per year, in a good year.

And that prompted me to look into liquidity. Why?

Making a return of +23.2% in a matter of few weeks is obviously great. That is, if one can realise the return, i.e. one can actually sell the asset, without affecting its price.

(Some crypto investors are learning this the hard way right now!)

So the question of liquidity is: how easily can one buy and sell this asset to realise this +23.2% return?

💦 Define liquidity

Liquidity risk is the risk of being unable to buy or sell assets in a given size over a given period without adversely affecting the price of the asset.

The shares of big companies (e.g. Apple) or indices (e.g. S&P 500) are traded cheaply in secondary markets, because they are part of a big pool of identical and interchangeable securities. Buy and sell orders can be effortlessly matched on electronic order books.

At the opposite spectrum of that there is, say, buying or selling a property. It might take anywhere between 3 months to one year because houses are idiosyncratic assets (no two are alike) and the process of buying and selling is lengthy, cumbersome and expensive.

Perhaps it is more helpful to think of illiquidity as an asset that cannot easily be sold to meet unexpected spending needs or to take advantage of other (better) investment opportunities.

Liquidity affords options, and illiquidity constrains them.

💹 The bid-ask spread = cost of trading

In addition to that, in markets for specialised assets (we should count wine amongst those), finding a suitable buyer or seller is costly. Generally, a wider bid-ask spread is needed to compensate for these search costs as well as for the risk of prices moving in the meantime.

It also takes effort and skill (read: cost) to appraise the value of idiosyncratic assets. There is a greater chance that your counterparty knows more about the asset’s true value than you do; so you may end up buying a lemon or selling a hidden gem.

Such risks add to the cost of trading less liquid assets and to the illiquidity premium that investors require to hold them.

In the wine world, Liv-Ex established itself as an exchange to streamline these trading operations and that made giant leaps in the ease of trading and its associate logistics operations, offering its members the infrastructure (data, trading and settlement) to significantly reduce the risk profile of the transaction.

However, consider that the bid-ask spread in the stock market is a few basis points (1 basis point = 0.01%), the average Liv-Ex bid-spread is far greater, making the fine wine market still a very illiquid market.

🌇 Illiquidity matters less if investors have longer horizons.

In 1986, Yakov Amihud and Haim Mendelson published a pioneering paper which posits that investors with the shortest horizons hold securities with the lowest trading costs; while relatively illiquid assets are held by long-term investors, who can spread the higher trading costs over a longer holding period. In principle, patient investors can reap a reward from illiquidity. But in practice the risks that go with it often prove to be bigger than many investors had expected.

Establishing the investment horizon is a critical element in understanding the kind of asset classes to invest in. And once that is settled — on an asset-by-asset basis — one needs to establish the exit trigger.

Returning to the case of my follower, if he were to believe that in the next year or two his Carruades 2021 investment would double as it is so wildly undervalued, then when either that time horizon is met or the value has doubled, he should sell.

💧 Liquidity varies over time as well as between assets.

Liquidity relies on the capacity of traders to supply it.

That varies.

In good times (read: in times of easy monetary policy), it is abundant. Asset prices are on a generally rising trend so traders find it easy to borrow to finance their asset purchases.

But in bad times, liquidity dries up. In extreme cases, such as the 2008-09 financial crises, there are self-perpetuating “liquidity spirals”: traders make losses on their assets; they are forced to sell assets to preserve their cashflow; and that in turn drives prices lower, further impairing their ability to trade.

At such times a lot of investors who were intent on picking up an illiquidity premium discover that they are far less patient than they had believed themselves to be back when liquidity was plentiful.

The possession of cash or the ability to raise it quickly is especially valuable in recessions. The skillful are able to pick up assets cheaply where others have been forced to sell. A short-horizon investor won’t buy such assets, for they might become even cheaper. But a truly patient investor who can wait for the payoff is able to step in—as long, of course, as they are liquid.

Going back to my follower’s case — chances are that a second wine, albeit from one of the first-growth châteaux, from an off-vintage (read: less-than ideal) would suffer in a recession or anyway in a down-market. Looking at the stock market for comparison’s sake — the stocks that work best (note: not losing money) in down-markets are for example utilities, safe and stable.

📉 The current environment and what does it mean for wine investment?

Central banks (Fed & ECB) have signalled a hawkish stance.

What does this mean?

The current environment isn’t ideal for collectibles as raising interest rates and other tightening tools used by central banks will have a negative impact on cash circulating in the economy and investment markets, which will dry-up the appetite for risk-on assets.

1️⃣ Raising interest rates and 2️⃣ Quantitative Tightening (QT) will increase the cost of borrowing and dry up liquidity in the pockets of the market that are considered ‘less safe’, with safer assets (bonds) becoming more attractive.

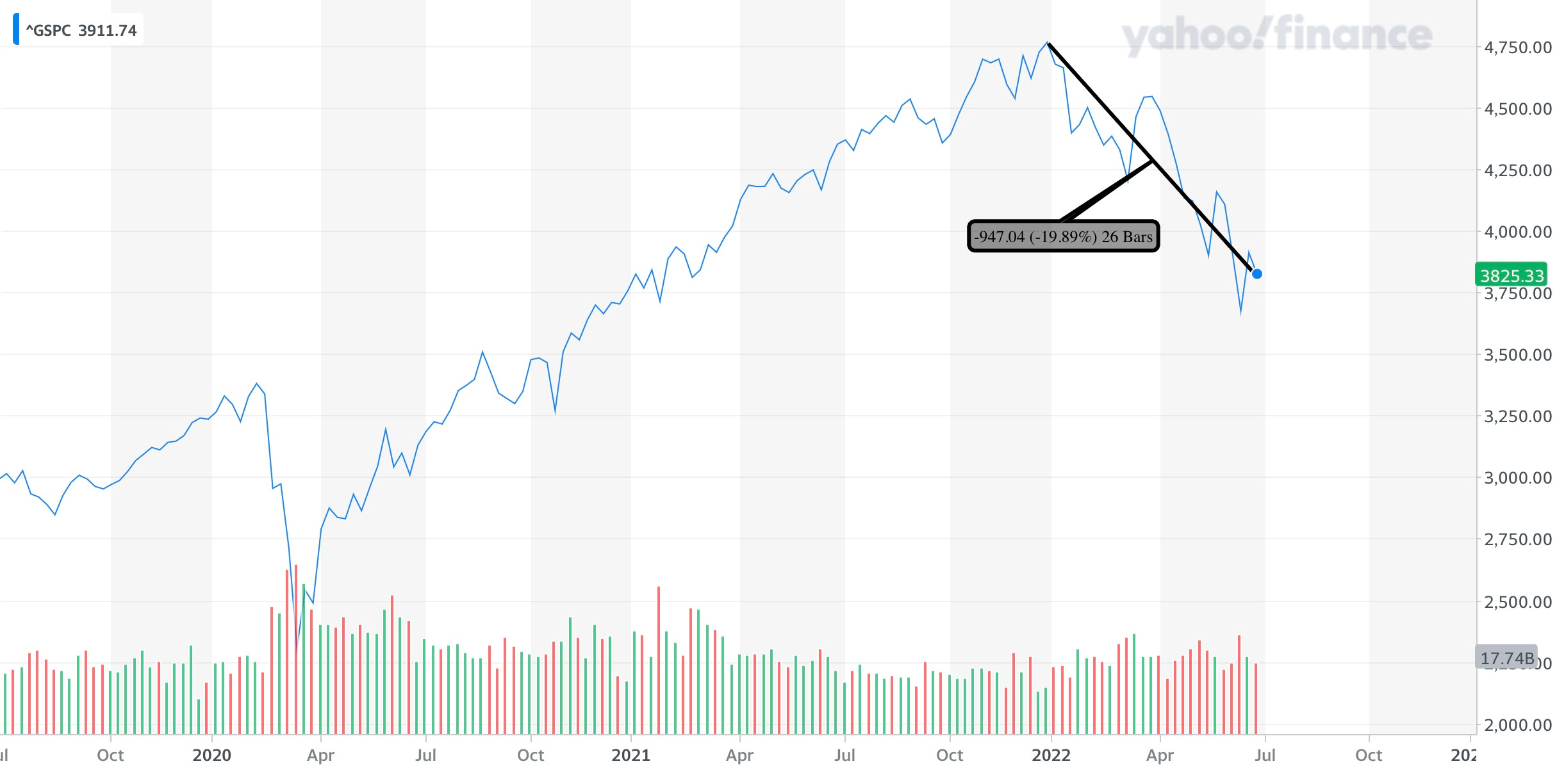

We’ve seen a little bit of that in the stock market, in the last six months:

↪️ Inflation is now upon us, and it’s even harsher than most central banks expected, in part due to the current Ukrainian conflict and in part due the supply-chain disruptions of 2021.

This means that central banks will act fast to contain inflationary forces from spiralling out of control.

As inflation rises, prices of wines and other assets will be pushed up — only to collapse in a year or two later when liquidity finally dries up as a consequence of the monetary and fiscal policies — the effects of inflation buoyed peaks (1971 to 1974 and 1977 to 1980) but were followed by a sharp decline in the following years.

If you glance at today’s fine wine market, I’d say we should be bracing for that sharp decline in the next coming years. Note that the two most recent corrections in market prices happened during the 2008 financial crisis and the 2011 European banking crisis.

🖋️ Final note

The key takeaway of this article isn’t that an illiquid asset is a bad investment.

On the contrary!

Investors with high levels of liquidity and a long-term investment horizon should invest in some well-appraised illiquid assets to take advantage of the illiquidity premium at times when such assets are trading cheaply.

However, the takeaway is that liquidity affects the ease and ability of selling an asset especially during recessions or else during times of monetary tightening (such as now).