Happy New Year wine lovers!

After a long break over the holidays, let’s take a quick look at what happened in 2022 in the wine market — and more importantly what to expect from the year to come.

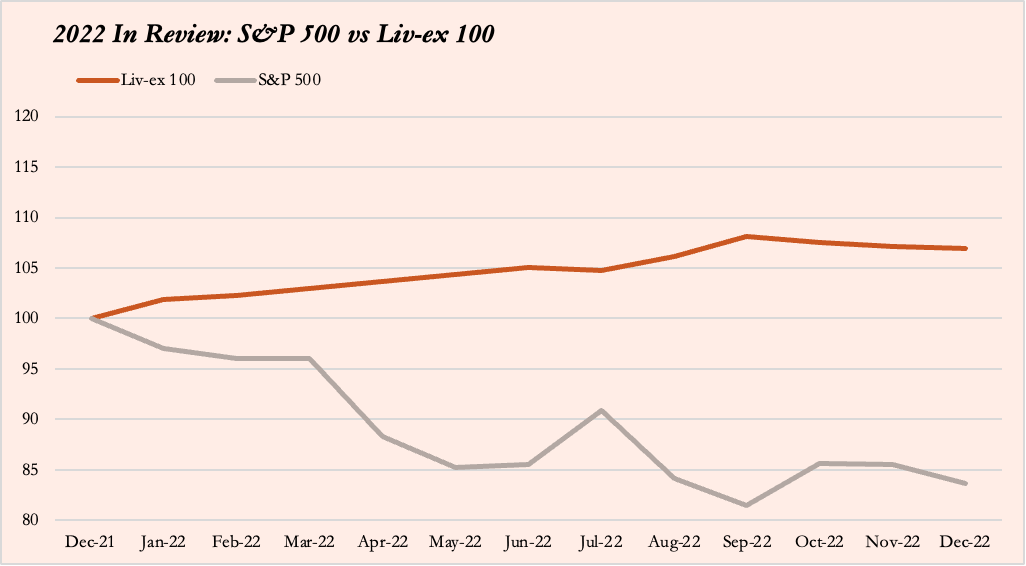

Those who invested in fine wine may feel smug right now — making 6% in absolute terms and 20% over a crippled 2022 stock market.

However, that’s not the full story: interest rates have seen the fastest acceleration, in terms of both magnitude and pace, since 1980 and 1981. Returns on bonds and deposits (virtually risk-free investments) have increased to 4-5%, justifying a flight to safer asset classes.

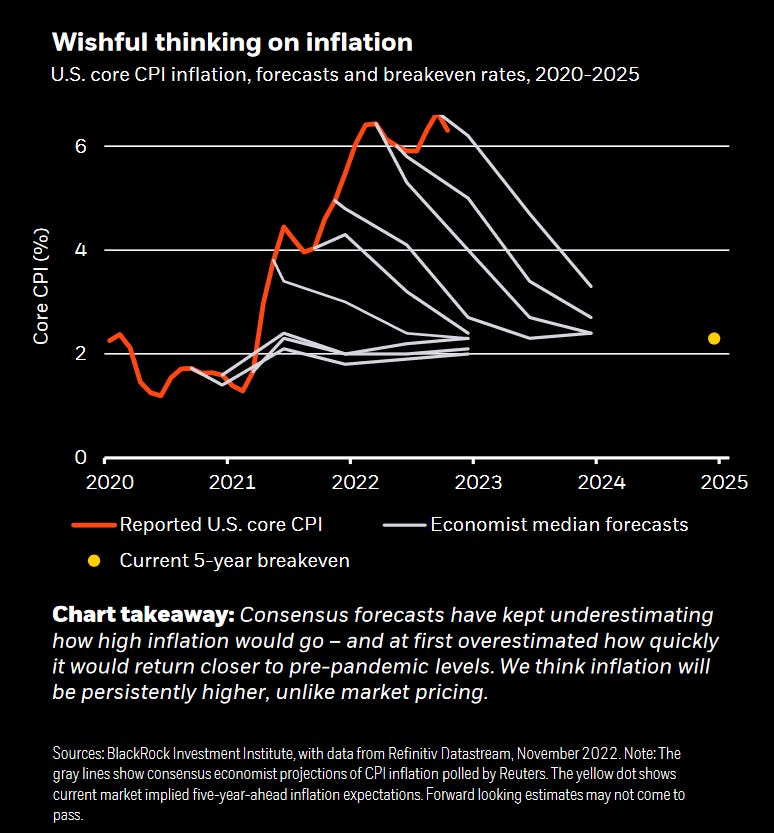

Inflation was at the centre of attention during 2022, especially since the Fed started increasing interest rates in March. It has certainly been more persistent than most economists predicted, as Blackrock’s chart below highlights.

2022 Fine Wine Market Recap

Split between the first part of the year (↑) and the second half (↓)

The fine wine market continued with its unrelenting climb in the first half of the year, which prompted many to hail wine as the best inflation hedge investment. However, the second half started showing signs of deceleration. Still a few wine-related (St-Emillion reclassification) and economic (the collapse of the £) events temporarily propped up prices in August and September.

St-Emillion Reclassification

The undisputed star of the St-Emillion 2022 reclassification was Figeac — finally promoted to well-deserved Premier Grand Cru Classé A. As Liv-ex highlights — Figeac dominated its competitors in the Right Bank, in terms of price gains.

Figeac index rose 7.9% in the month prior to the announcement: many bet on its promotion. Since then however, the composite Figeac index didn’t move, undoubtedly because most of its gain were already discounted and some of it because of a stagnant fine wine market.

Figeac 2019 (a holding in the Saturnalia Model Portfolio) went from £141 / bottle to £212.5 / bottle (+50.7%) in a matter of weeks, which prompted me to review my position and ultimately sell half of the position at the end of October.

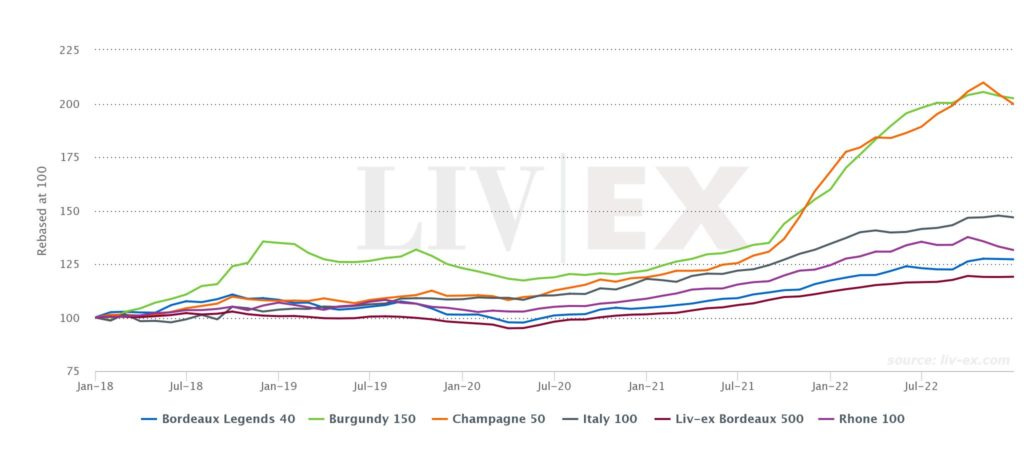

Unstoppable Champagne & Burgundy

Eight out of Liv-ex top-10 performers in 2022 were Burgundy or Champagne. In 2022, Liv-ex Burgundy 150 (+26.7%) and Champagne 50 (+18. 7%) outperformed by at least 15% most of other wine regions.

Why? Back in January 2022, William Kelley correctly predicted this buoyant market for Burgundy, highlighting the biggest drivers.

What of the market for 2020 Burgundies? Early indications are that we’re witnessing a perfect storm: insatiable demand from affluent buyers who want to acquire the wines no matter the price, notable increases in ex-domaine tariffs and the prospect of an extremely short crop in the 2021 vintage are combining to drive Burgundy prices to new heights. Is this likely to precipitate some sort of crash in the near future? I don’t think so, as for now there appear to be plenty of consumers willing to open and drink bottles at these prices. But it will certainly stimulate reflection among producers about how they can better control the distribution of their wines, both to capture more of the value of their product and to ensure that their wines end up in the hands of genuine consumers, not speculators. On the consumer side, the soaring prices of the most sought-after wines of the Côte d’Or will surely be an incentive to look at less glamorous appellations more seriously; and as I have argued in these pages on numerous occasions, careful shoppers looking for bargains will find excellence as well.

As far as Champagne is concerned, Six Atmosphers’ Tom Hewson and I tried to make sense of the market. Bloomberg even says that a large increase in Champagne prices is a forward predictor of recessions. However, one of the most convincing reasons for the excitement has more to do with specific dynamics to Champagne: the rollout of vintages and stock levels. Tom Hewson explains:

It looks like the only vintage since 2013 likely to go down as a classic will be 2019. Furthermore, a number of these were badly frost-affected, so quantities of whatever Prestige releases there are may be relatively small. What’s more, with the exception of some 2014s, none of these vintages promise a cool, long-lived character; at best they are likely to come out rather sunny and generous. […] Perhaps investors know that we may all be feeling a little starved of top vintages in a few years’ time.

What does 2023 have in store for us fine wine lovers? Here’s a few predictions.

Prediction #1: Burgundy EP 2021 is scarce & pricey still

Taking a look back at 2021 in the Burgundy vineyards, it was one of the most difficult growing seasons in living memory and it will be remembered for the frost in the first week of April that decimated the crop.

Early spring budburst

Hard frost in spring followed by snow

Rain and cool temperatures resulted in mildew & grey rot

Not very warm until August

September was not hot, but it was warm enough to drag the small crop of fruit that remained on the vines to sugar levels and potential alcohols that were halfway decent.

Quality? While the frost decimated the quantity, cool weather made critics and winegrowers worried that tannins may be a bit ‘vegetal’ and the wines may be a bit thin and unidimensional. Jancis Robinson said it will be a comeback to cool-weather Burgundy, with some doubts over their longevities. Most of the drinking windows are 10 - 15 years.

Prices? There doesn’t seem to be an end to price increases in Burgundy. The EP 2020 saw a huge increase in prices, many said because it was to make up for what was an already disastrous 2021 vintage. But of course, this year EP prices increased still. So far, offers from Lay & Wheeler, BBR & Jeroboams (and others) have somewhat disappointed. Some of the allocations may be certainly up a notch — but it won’t make up for the horribly tiny quantities and yet another ~25% price hike.

Not only have I purchased the membership for Jasper Morris - Inside Burgundy, but I’ll also have the chance to taste a few from some merchants in the coming weeks. Stay tuned for individual names.

Prediction #2: Look out for that Barolo 2019

If you want to allocate some $$$ in fine wine, make sure you reserve some for the excellent forthcoming vintages from Piemonte, 2019 Barolo and 2020 Barbaresco.

While winegrowers in Barolo are currently dealing with the effect of climate change, specifically the horribly dry and desert-like conditions of 2022, the vintage presented at the Grandi Langhe on 30th-31st January will be the much-awaited 2019.

More on that in February 2023.

Prediction #3: Brace for a desert-like Bordeaux EP 2022

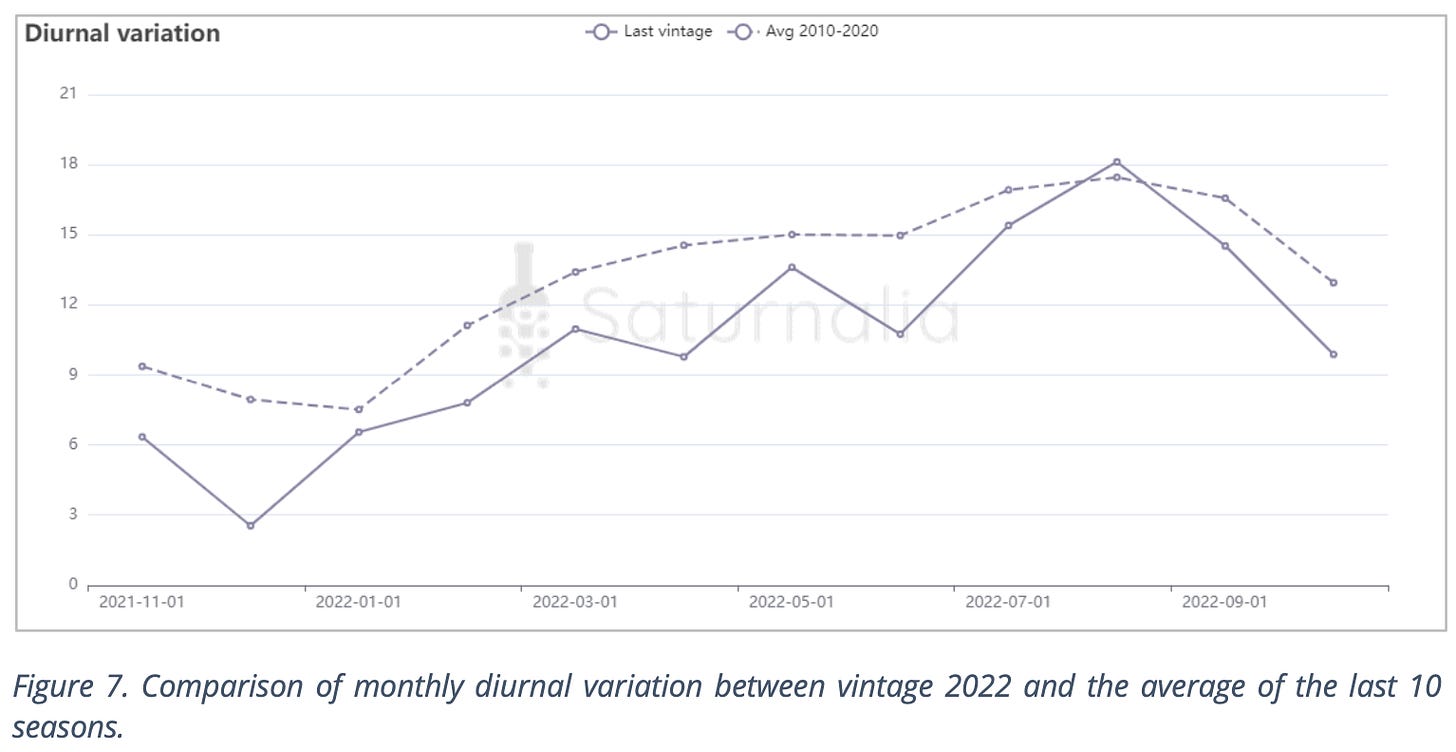

While tastings of the barrels won’t happen until late spring, Saturnalia already published its predictions based on rainfall, average temperatures, diurnal range, and their own proprietary models.

Summarise 2022 in a few words? Dreadfully hot and dry.

Water stress had an impact on berry concentration

Nights weren’t cool = low diurnal variation could cause the loss of freshness and acidity in grapes.

Source: Saturnalia Looks like similar conditions as 2020 but slightly worse

I think these charts tell most of the story. SVI maps are developed using satellite images that give an objective view of the water content of the vine overlayed with Saturnalia’s proprietary mathematical model. Without going too much into details — yellow and brown spots on the map indicate that the vine may be in water stress, in this vintage because of the desert-like conditions. The top image in each shows the 2022 vintage, while the one underneath shows the same map for 2021. It’s clear that, across each appellation, a much larger portion of vineyard was in stress compared to the previous year.

The least affected appellation was St-Emilion.

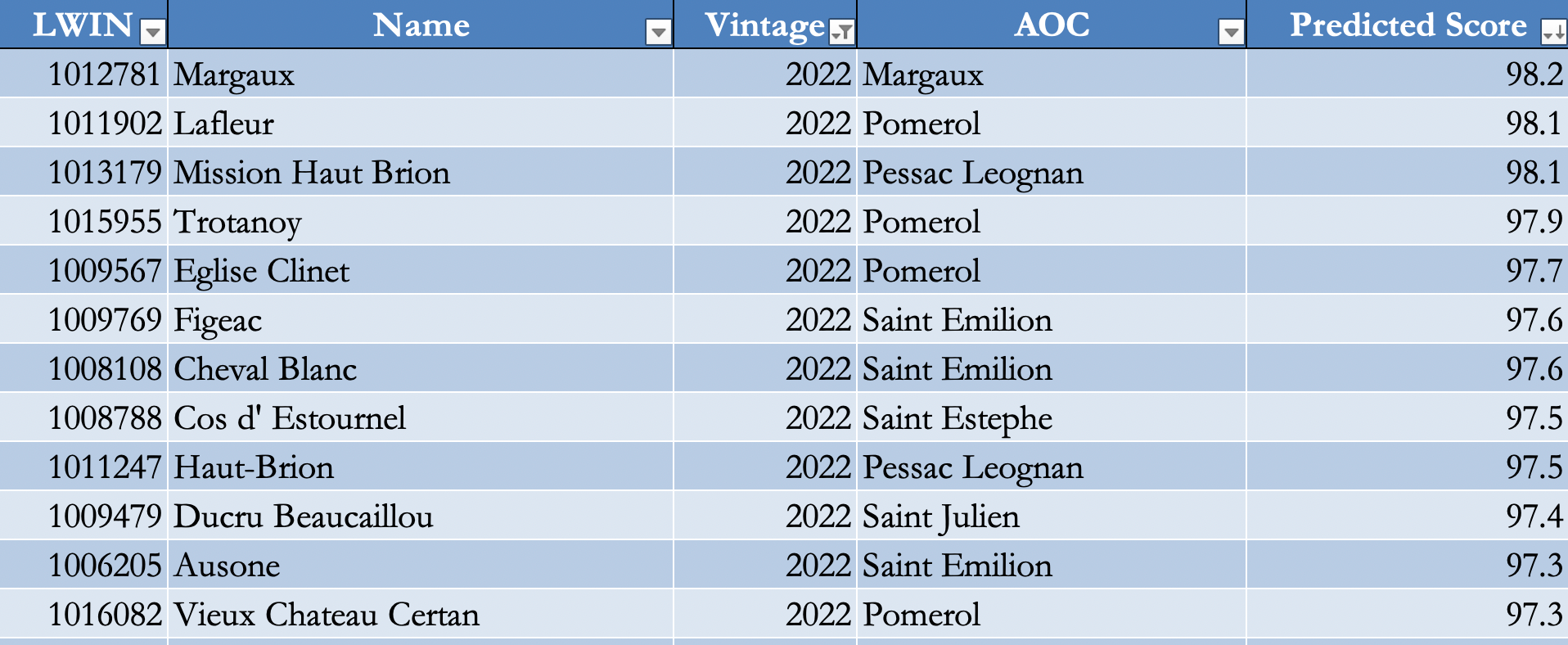

Interestingly, Saturnalia also predicts a score for the EP 2022 wines, even ahead of the wine critics tasting and releasing their opinion.

How?

They simply use a machine learning model that accounts for past performance, brand recognition and current vintage condition, specifically to each châteaux, to come up with a predicted score. It’s surprising to see many château in appellations that may have suffered — but their reputation for high-standard and the location of their plots specifically may be the reasons. Nonetheless, I’d still bet on St-Emilion’s names.

Despite the desert-like conditions of the vintage, potential smoke taint issues are what makes me the wariest. Back in July, the CIVB wine bureau said that no vineyards had been impacted and that consultants were cautiously optimistic. That seems to be odd as Jane Anson wrote that even in central Bordeaux “they can smell and see the smoke”, then adding that “it is so strong that you can’t help but check and recheck your house for burning, before heading outside and seeing clouds of smoke hanging over the entire city.“

Smoke taint occurs when developing grapes are exposed to the smoke from wildfires for any period of time. A number of factors will determine the level of impact the smoke will have on the berries, including berry development, duration of exposure, and concentration of smoke.

Smoke taint is insidious — as Lisa Perrotti-Brown pointed out — because “volatile compounds from smoke contact bind with sugars, forming more stable compounds known as glycosides. Glycosides are non-volatile, meaning that they can’t be smelled or tasted. Glycosides are, however, somewhat unstable. Contact with acids or enzymes can break the bond, and the smoke compound becomes detectable again. This bond can become undone during fermentation, when a wine has been in bottle over a period of time, or when the wine comes in contact with enzyme-containing saliva. Thus, smoke taint can exist masked in wine for a period of time before it becomes apparent.”

Here’s a list of some of its effects on wine:

unpleasant classic aromas of campfire, ash and wood smoke on the nose and palate, with a persistent aftertaste long after the fruit has disappeared

tannins appear harder and more astringent

elevated levels of perceived alcohol

the wine lacks character and complexity

severely impacts longevity

Although skeptical, the true test will come from the EP season, which I’ll follow closely. It could be the case that many châteaux prefer using non-affected grapes and make their first wine in smaller quantities… More on this in May/June.

Prediction #4: Champagne on ice…

As incredible as it sounds, the Champagne 50 was the worst performer, down 2.4% in December, and for the second consecutive month in a row.

What’s more telling is that December is normally a great month for bubbles in general, which could be a signal of cooling-off. Not to despair — it could be a great chance to pick up some bargains.

Prediction #5: Is the Fine Wine Market Finally Softening?

Overall, I don’t think releases expected in 2023 will enthuse anyone, with of course few exceptions from Piemonte.

On the economic side, many investors and economists predict a likely recession. Others think that the cycle of outsized rate hikes will stop without inflation being back on track to return fully to 2% targets — a view that offers better prospects. Either way, we are staring in the eyes of a recession if inflation has to come down, which may not be as severe as 2008-11, but still.

These two factors combined may pull the breaks on the fine wine price rally that dominated the narrative in the past 2 years. Finally, I might add.

It won’t be a good time to offload some of your cellar but at the same time, it may be a good time to pick some gems.

Performance

Let’s have a look at the Saturnalia Model Portfolio performance.

In the four months since its inception (8 September 2022), the Saturnalia Model Portfolio returned 2.7%. During the same period, the Liv-ex 100 gained 0.73% and the Liv-ex 1000 (a broader index) was up 1.38%.

Focussing on the month of December the portfolio lost ground finishing at -0.4% (vs -0.2% of Liv-ex 100) on the previous month.

The negative performance was largely driven by Ausone 2016 (-1.5%) and Figeac 2019 (-4.1%). On the other hand, positive performance was driven by Canon 2019 which gained 12.3% in the month of December.

Please note that I calculated the portfolio return ex-cash. That’s because the ‘cash allocation’ is not strategic but it’s a £50,000 yearly budget allocated to fine wine investing, perhaps in the same way that some wine collectors/investors think about their yearly portfolio allocation to fine wine.

We already discussed why Figeac 2019 may see some softening in the coming months and years: large gains following their promotion may retract somewhat, especially if the fine wine market as a whole starts softening.

Ausone 2016 lost 1.5% in December — a small amount; however because of the high price per case, Ausone represents 13.4% of the total portfolio. This means that small movements in the price have a larger impact on the performance of the overall portfolio.

Canon 2019, which I had bought anticipating an upgrade to 1er GCC A, didn’t. However, many investors (such as myself!) may be looking at Canon (and in particular the 2019 vintage) and think it’s a great bargain! We may see more of those value-driven investments in 2023.

In the coming months, and in light of the somewhat disappointing releases ahead of us, I’ll be scouting for some past vintage gems to add to the portfolio. I’ll be sure to share them with you.

Happy New Year!

Thanks for reading In the mood for wine — it’s a privilege sharing my thoughts on fine wine with like-minded wine lovers. If you found this article interesting, why not share it?

Regards,

New? Sign Up Here

Got Feedback? Just Hit Reply

IG: In the mood for wine / Twitter: In the mood for wine

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and significantly different from those of my readership. As such, the investments covered in this publication and in this article are not to be considered investment advice nor do they represent an offer to buy or sell securities or services and should be regarded as information only.