You know I love ChatGPT, perhaps as much as I love Saturnalia, if that’s even possible!!!

In the last week, ChatGPT released a new Code Interpreter (available only to us Plus members, of course). Using this new plugin, one can upload data and then ChatGPT will analyse it with plain English commands. So, I decided to test it to see if it can discern what trends in the Liv-ex 100 were telling us about its likely path, based on financial technical analysis. Specifically, I want to understand if the fine wine market has reached its bottom, if it’s oversold and if so, which pockets of the market look the most attractive. I’ll look at it within the context of the Saturnalia Model Portfolio, built using the Saturnalia wine investment platform.

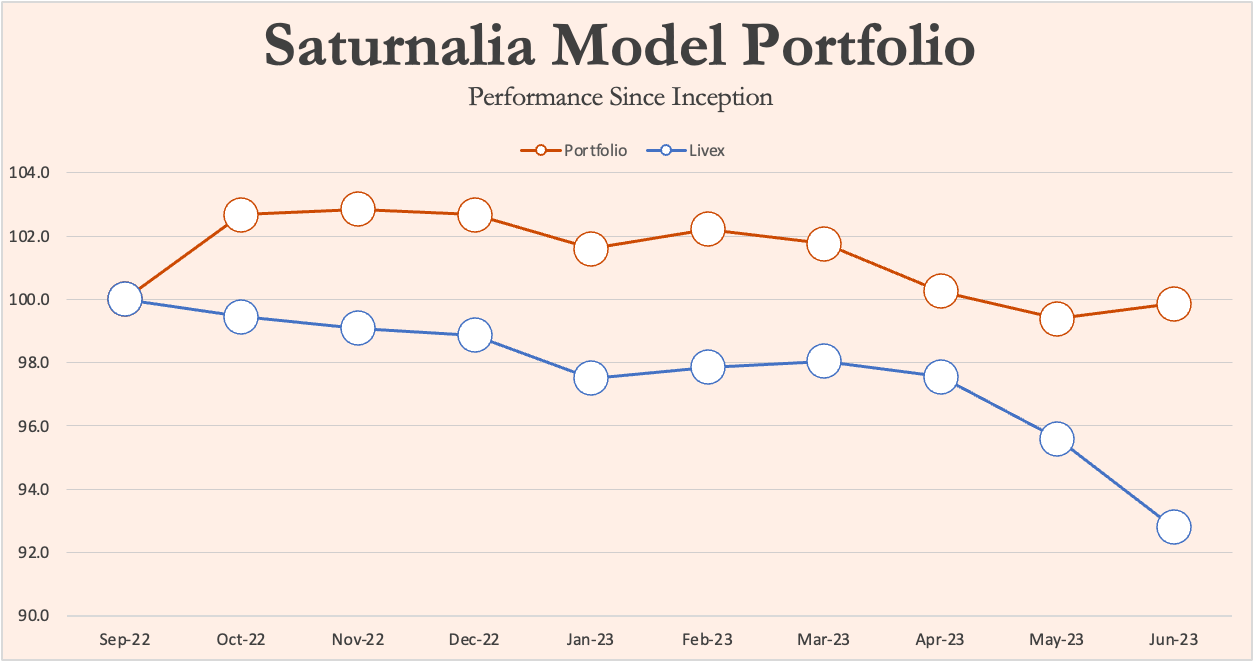

The Saturnalia Model Portfolio (excluding cash) saw an increase of 0.8% in June 2023. During the same timeframe, the Liv-ex 100 experienced a decrease of -2.9%. Comparatively, the portfolio surpassed the index by 3.7% — demonstrating that at times, inaction can indeed be the most effective strategy.

What happened in the fine wine market?

The market is evidently contracting — the Liv-ex Fine Wine 100 (the industry standard) decreased by 2.93%, reaching its lowest point since December 2021. As we noted last month, the Liv-ex 100 fell below its support line, suggesting a change in market sentiment and a possible significant shift in the market's trend.

The question is, how low can the fine wine market go?

Here’s what I asked ChatGPT:

Here is the monthly time series for Liv-ex 100 going back to 2001. Can you analyse it using technical analysis to interpret the next likely move of the index?

ChatGPT response really impressed me.

(Copy & Pasted below)

The data appears to contain two columns: "date" and "Liv-ex". The "date" column contains the timestamps for each data point, and the "Liv-ex" column contains the corresponding value of the Liv-ex index.

To conduct a technical analysis, we will:

Visualize the time series data.

Identify any trends or patterns, such as upward or downward trends, cyclical patterns, or significant spikes.

Apply technical analysis indicators, such as Moving Averages (MA), Exponential Moving Averages (EMA), Relative Strength Index (RSI), etc.

Interpret the results of these indicators to predict the next likely move of the index.

Let's start by visualizing the time series data.

The plot shows the Liv-ex index over time. There are clear upward and downward trends at different periods. We can also see that the index experienced significant growth after around 2005, followed by a steep decline during 2008-2009 (most likely due to the global financial crisis), then a rebound and a fairly stable period after around 2015.

Let's now apply some technical analysis indicators to this time series. We'll compute:

The simple moving average (SMA) with a window of 12 periods. This will help us identify the overall trend in the index.

The exponential moving average (EMA) with a window of 12 periods. EMA gives more weight to recent data and thus responds more quickly to price changes.

The relative strength index (RSI) with a window of 14 periods. RSI is a momentum oscillator that measures the speed and change of price movements. It is primarily used to identify overbought or oversold conditions in a market.

After calculating these indicators, we'll plot them alongside the original time series to help us interpret the data.

The above plots present the original Liv-ex index data along with the Simple Moving Average (SMA), Exponential Moving Average (EMA), and Relative Strength Index (RSI).

In the first plot, the SMA and EMA provide a smoothed version of the original data, helping us to identify the overall trend. The EMA being more responsive to recent changes can be seen as it diverges from the SMA during periods of volatility.

The RSI is shown in the second plot. This is an oscillator that moves between 0 and 100. A common interpretation is that an RSI over 70 suggests the index is overbought (and may be due for a price fall), while an RSI under 30 suggests the index is oversold (and may be due for a price rise). The 50 level is often seen as a confirmation of a trend; above 50 is considered an uptrend, and below 50 a downtrend.

To determine the next likely move, let's analyze the most recent data:

The last point of the Liv-ex index.

The last points of the SMA and EMA.

The last point of the RSI.

The most recent data is as follows:

Liv-ex index: 393.82

Simple Moving Average (SMA): 414.43

Exponential Moving Average (EMA): 407.88

Relative Strength Index (RSI): 38.22

Let's interpret these numbers:

The last value of the Liv-ex index is below both the SMA and EMA. This indicates that the recent movement has been downward, as the index is lower than its average over the past 12 periods.

The RSI value is below 50 but above 30. This suggests that the index is somewhat oversold but not extremely so. It may indicate a potential for price increase, but it's not a strong signal as it's not below 30.

In summary, technical analysis suggests that the Liv-ex index has been in a downtrend recently. However, the RSI indicates that it may be approaching oversold conditions, suggesting the possibility of an upward reversal in the future. However, these indicators should be used in conjunction with other forms of analysis, such as fundamental analysis, to get a complete picture of the market conditions.

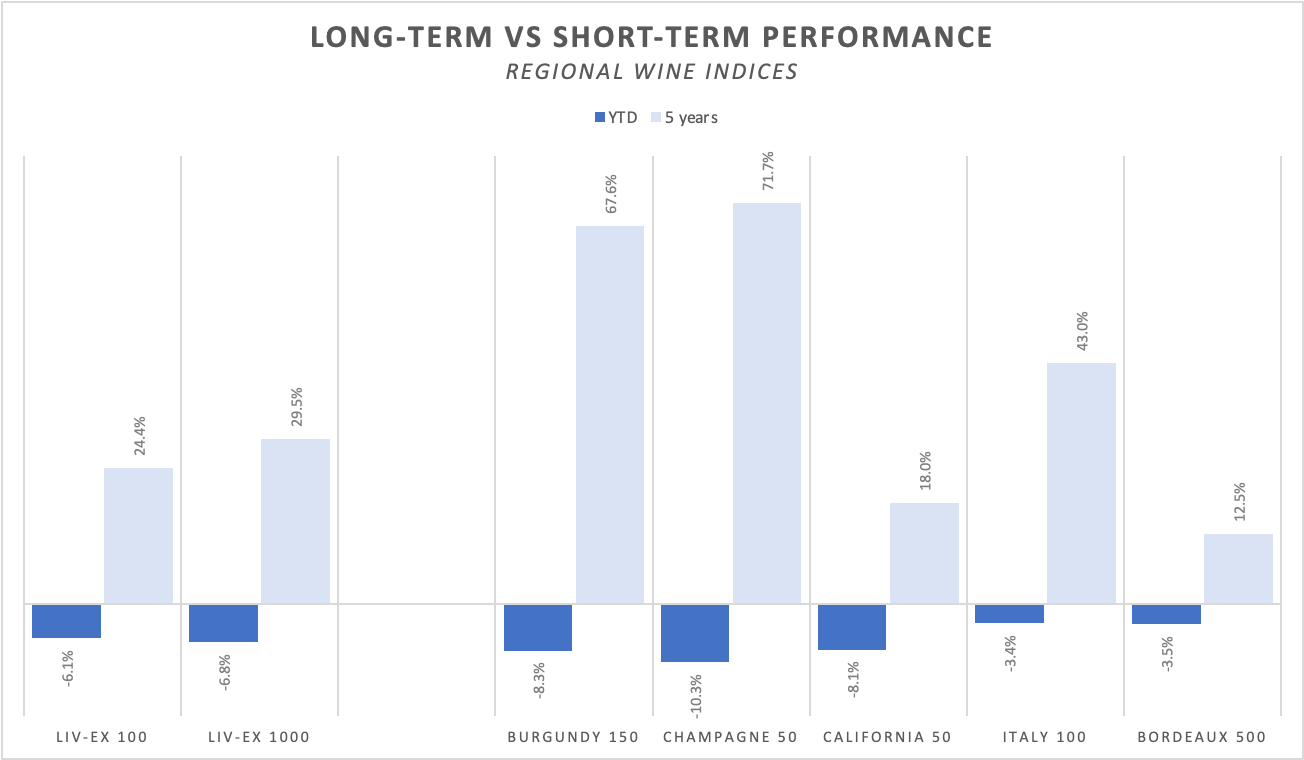

I conducted the same experiment with the Liv-ex 1000 and the results were strikingly similar. (It's worth noting the difference between the two indices: the Liv-ex 1000 has a broader scope as it tracks the performance of 1000 wines instead of 100).

What ChatGPT is suggesting about the market is that the fine wine market is nearing its lowest point, but it hasn't quite reached it yet. However, timing a market bottom (the point at which asset prices have hit their lowest before starting to rise again) is notoriously challenging, and it's generally considered virtually impossible to do so consistently and accurately.

In addition to examining indicators like the Relative Strength Index (RSI), which aids in detecting an oversold asset, or like trading volume (a metric that Liv-ex does not openly disclose), or observing when the price surpasses a significant moving average as a signal of a trend reversal, there's also Sentiment Analysis. This method identifies periods of intense negative sentiment, which often align with market bottoms and relies on the contrarian belief that when the general mood is pessimistic, it could be an opportune moment to invest.

Sentiment in the fine wine market has crossed pessimist to reach to sour. Although looking at the average critic scores, the 2022 vintage ranks higher than any other dating back to 2005, the Bordeaux En Primeur 2022 has left many collectors puzzled and hasn’t helped drive interest in the vintage or the region.

A similar sentiment is evident in the 2014 and 2015 Champagne releases, which were priced higher than the Champagne houses’ respective 2013s.

Collectors have stood their ground and shown that they are not ready to buy at any cost.

Now, let's examine the performance of each region to see if any are more poised than others for a rebound.

Burgundy 150

Burgundy shook collectors with its dramatic price surge, so much so that The Economist declared a bubble in 2019. From the time of that article until the index peak in October 2022, the Burgundy 150 soared an additional 60%.

Despite arguments of limited supply, the price trends in the region have been largely propelled by a surge in demand from Asia. However, recent macro-economic data suggests that Asia may not continue to support these high prices as it has over the past decade.

Technical analysis shows that the Burgundy 150 is currently in a downward trend, recording a significant drop of -8.3% since the start of 2023 and -9.6% from its peak.

Some of it could be down to seasonality, as Burgundy En Primeur takes places in the second half of the year. The 2021 could be an interesting vintage to watch in the Côte d’Or — not one for the annals, as pHs are on the high side, but “[ … ] supple, fleshy and perfumed, at their best uniting the concentration of low yields and surprisingly good phenolic maturity with the vibrant, perfumed profiles of a cooler vintage. Their pHs are relatively high, so the wines are broad, open and charming. They’re unlikely to shut down. A cleaner, more concentrated version of the 2000 vintage“ writes William Kelley in The Wine Advocate.

Given that producers in the region have been steadily increasing release prices each year, if they take cues from recent Bordeaux and Champagne releases, there might be opportunities for astute collectors.🤞

Champagne 50

A quick look at the regional chart above shows that Champagne, as measured by Liv-ex, has experienced the most significant fluctuations, ranging between its long-term performance (+71.7%) and its year-to-date (2023) correction (-10.3%).

Technical analysis indicates that the Champagne 50 index is currently on a downward trend. However, the Relative Strength Index (RSI) suggests that it might be nearing oversold conditions, though it hasn't quite reached that point yet.

Among the Grandes Marques Champagnes, the 2013 vintage stands out as a potential value buy. I've explored this topic further, along with recent releases in Champagne, in a guest article for Six Atmospheres.👇🏼

Out of all the regional indices, the California 50 (which encompasses 10 vintages from Dominus, Harlan Estate, Opus One, Ridge, and Screaming Eagle) appears to be the most oversold, with a Relative Strength Index (RSI) of 28.57. A figure below the 30 threshold is frequently seen as a bullish signal, suggesting a potential for a price increase.

To put it simply, now is an excellent opportunity to invest in Californian wines.

But which ones should you consider?

Among the California 50's worst 12 performers over the past year, eight are from Screaming Eagle and three are from the challenging 2011 vintage.

The 2011 vintage in Napa Valley was particularly difficult, surrounded by three spectacular vintages. From a pricing standpoint, it may not be worthwhile to consider 2011, as the prices do not seem to account for the challenges of that year.

In contrast, the adjacent years 2010, 2012, and 2013 are celebrated for their exceptional quality, producing a wealth of world-renowned wines. When considering age, the 2012 and 2010 Screaming Eagle vintages currently trade at similar prices.

Sticking with Screaming Eagle, the 2015 vintage appears to be a better deal than its 2016 counterpart, although neither seems to be a particularly cheap option.

In terms of value, the Dominus 2018 features prominently.

Italy 100

Italy presents a conundrum. While the Italy 100 index has quadrupled in the past two decades, Italian wines, with the exception of a few well-known Super Tuscans and a handful of Barolos, often struggle to find traction in the secondary market. The absence of an En Primeur system likely contributes to this situation.

Could it be that collectors prefer to actually consume Italian wines compared to their French counterparts? 🤷♀️

It's unsurprising, therefore, that Italy's regional index has shown the least price volatility. This stability is likely aided by the release of the impressive Barolo 2019 vintage earlier this year at reasonable, balanced prices, as well as the impressive Bolgheri 2020.

While I may be showing a bit of bias here (🇮🇹🤌), I firmly believe that some Barolos, Barbarescos, and Tuscan wines currently offer the longevity that top collectors expect, but at more competitive prices compared to their French counterparts.

Liv-ex reported that the average release price during the En Primeur campaign rose by 20.8% compared to 2021, a stark contrast to the 7% increase that Liv-ex members had forecasted. Interestingly, even before the campaign had concluded, offers on the market were appearing at up to 15% lower than their opening price.

Liv-ex indices don't include any En Primeur wines or wines that haven't been bottled yet. However, as Liv-ex noted, this represents "another missed opportunity", not just to provide working capital for châteaux that need it, but also to draw the attention of new and younger generations of collectors to current or previous vintages.

Final Thought

It's evident that the fine wine market is currently in a significant downturn.

However, it's less obvious whether we've hit rock bottom and can expect a rebound in prices anytime soon.

Based on my understanding, I believe we haven't reached the bottom just yet.

Firstly, I don't see any imminent releases that would stimulate the market enough to reverse the prevailing negative sentiment.

Secondly, collectors haven't adapted to the inflation-adjusted release prices, and the Bordeaux EP campaign did little to help.

Lastly, on a macroeconomic scale, persistent inflation continues to rise in most of the wine-buying regions; the UK and a large part of Europe are likely to face an economic slowdown in the next year or two. This is not promising news for luxury markets such as fine wine.

What’s your view? Let me know!

Loading...

As always, thanks for being here!

This newsletter is free for all readers and the best way to keep it free is to subscribe, re-share it with your wine-lover friends, and follow me on Instagram.

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different from that of my readership. As such, the investments covered in this publication and in this article are not to be considered investment advice nor do they represent an offer to buy or sell securities or services, and should be regarded as information only.

Great writing and insight as always! I love the nuanced use of GPT! In AI we trust :P