My Fair Value a.k.a. Is Cheval Blanc Undervalued?

Unveiling the True Worth of Bordeaux 2022 in Three Acts

Hello wine lovers,

In the world of finance, where numbers dance and markets sway, it's time to meet "My Fair Value". Just as Eliza Doolittle blossomed under Professor Higgins' guidance, investors seek the fair value that reveals the hidden potential of their financial endeavours.

The Fair Value unravels the intrinsic worth of an investment; it transcends the ephemeral market fluctuations, guiding investors towards a more accurate evaluation; it harmonises the fundamental aspects of an asset, painting a vivid picture of its true worth. It represents the price at which an asset should theoretically trade in a perfectly efficient market, where buyers and sellers can access all relevant information. Or at least, that’s the goal.

However, determining fair value is not always straightforward, as it requires making assumptions and judgments based on available past information, which can introduce some subjectivity into the process — each investor has various valuation techniques, such as discounted cash flow analysis (more for stocks than wines…), comparable market analysis, or the use of mathematical models, considering factors such as future cash flows, risk, growth prospects, and market conditions.

In a recent article, Dr Philippe Masset, an Associate Professor of Finance at the École Hôtelière de Lausanne, delves into the concept of Bordeaux Fair Value and shares insights from his own model. Specifically, he explores the fair value of this 2022 Bordeaux season, which I’ll look at within the context of the Saturnalia Model Portfolio, built using the Saturnalia wine investment platform.

You can read the background of this project here:

Portfolio Performance

The Saturnalia Model Portfolio (ex-cash) retracted by -1.5% in May 2023. The Liv-ex 100 also fell by -2.0% during the same period. In relative terms, the portfolio outperformed the index by 0.5%.

What happened in the fine wine market?

The market is softening again — the Liv-ex Fine Wine 100 (the industry benchmark) was down 2% to its lowest level since March 2022. Not only that, but also the Liv-ex 100 broke below its support line, indicating a shift in market sentiment and a potential decisive change in the market’s trend.

Breaking a support line is often seen as a bearish signal, suggesting that selling pressure has increased and buyers are less willing to support the market at higher prices. It may trigger additional selling as investors perceive the breach of support as a signal to sell their positions or avoid entering new positions.

You may have noticed that I haven’t added wines to the portfolio in the last few months — that’s because I was expecting a stronger signal that the market was going one way or another.

This, once again sets the stage for …

…En Primeur 2022

The sentiment surrounding the current En Primeur campaign is marked by confusion. Some view it as tedious and erratic, while others struggle to comprehend it. In the last pool, 83% of you said they haven’t bought EP and they don’t intend to — not a scientific survey, but it sets the mood.

Some châteaux might deliberately overprice their wines to safeguard or enhance their brand value in a challenging fine wine market. Despite a decline in Liv-ex indices, release prices continue to climb. The original appeal of En Primeur, acquiring wines at the lowest price, is questioned given improved storage conditions and the availability of ex-château stock of excellent quality.

Although many fine wine collectors have already formed their opinions on current pricing, it is worth delving into the use of mathematical models to assess whether they have made the correct decision.

Step 1: A Financier's Elocution Lessons

To ascertain fair value, financiers embark on a journey akin to Professor Higgins' elocution lessons. They meticulously analyze market data, scrutinize financial statements, and decipher economic indicators. This step is crucial, akin to refining Eliza's speech, as it lays the foundation for uncovering the investment's underlying potential.

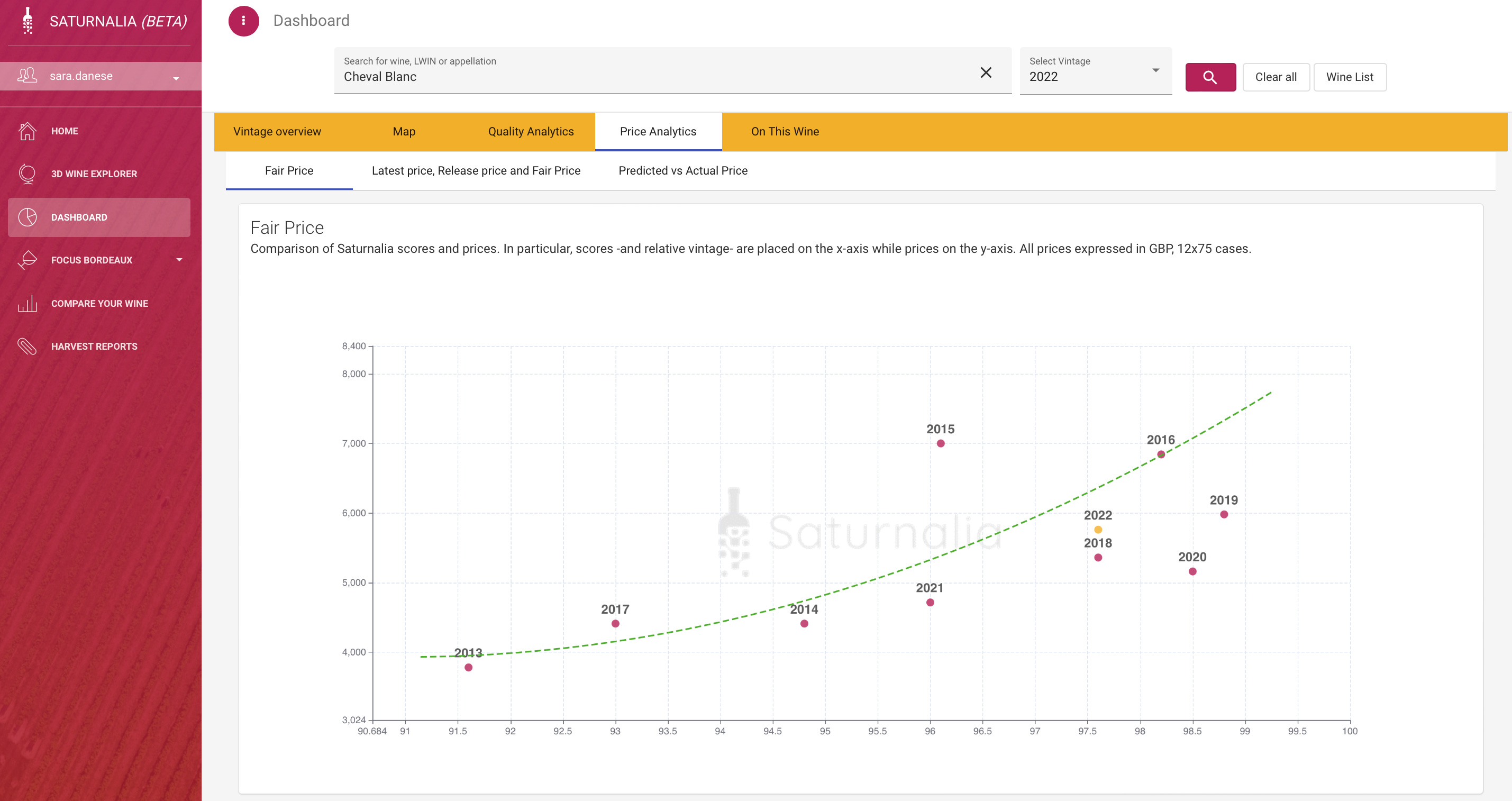

Dr Philippe Masset’s model uses regression analysis to estimate the relationship between the price of wines already on the market and three variables: quality, age, and château reputation. The analysis distinguishes between Premier Crus Classés and other Bordeaux crus, taking into account expert ratings and the quality of the vintage.

Quality of the wine (↑) is defined by a combination of three scores: Global Wine Score (GWS), The Wine Advocate (TWA) and Saturnalia (SAT).

Age (↑), the older the wine (the more ageing the wine underwent), the more valuable it becomes.

Château reputation (↑), thanks to their special status, first growths and alike are clearly more expensive than all other crus.

Step 2: A Market Ascot Opening

Just as Eliza made a stunning entrance at the Ascot races, fair value unveils itself on the market stage. Here, investors witness the convergence of market sentiment and fundamental analysis. It's a grand spectacle where fair value emerges, captivating the crowd and separating the gems from the ordinary.

This analysis brought to our attentions, these three facts:

The wine critic effect is weaker for established premier cru names with scores close to or below 95 points. Scores close to 100 points translate into clearly higher prices.

Ageing translates into a price increase of around 2% per additional year of cellaring for Premier Crus Classés, while for other wines, the effect is just over 4% appreciation per year in the cellar. This effect accumulates over time, leading to substantial premiums for wines aged 10 years or more.

Here’s the pecking order of Bordeaux châteaux:

Step 3: The Enchanting Transformation

In the final act, fair value works its magic, transforming an investment into its truest form. Similar to Eliza's metamorphosis into a refined lady, fair value brings forth the investment's hidden attributes, including its growth prospects, cash flows, and long-term potential. It guides investors towards wise decisions, enabling them to embrace the allure of undervalued assets.

The result of Dr. Masset are truly enchanting indeed. To my surprise, the model found that Cheval Blanc 2022 was released at a discount.

What? Really? How?

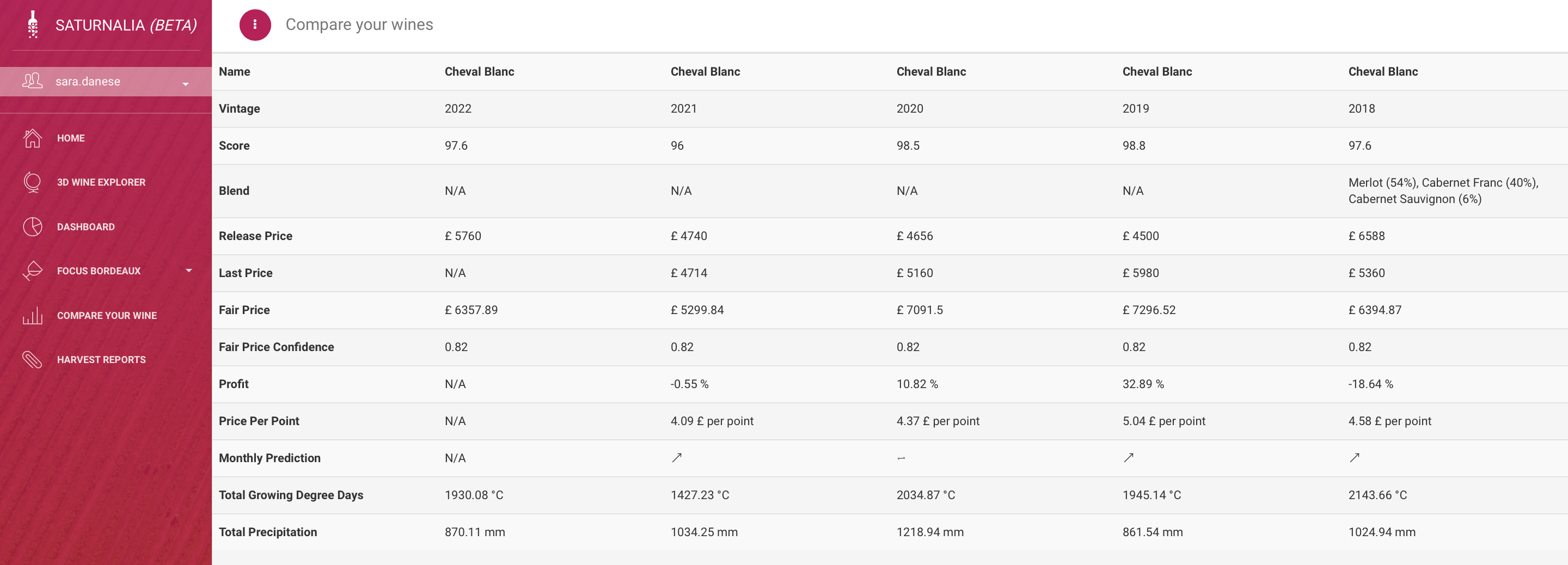

In the last article, we analysed both Angélus and Cheval Blanc👇

The earliest harvest ever

Hello wine lovers, En Primeur 2022 started with a ˗ˏˋbang´ˎ˗ Or more like, with a 30% increase in prices. Will other châteaux follow suit? Will there be an appetite from collectors for this 2022 vintage? I’ll share my financial thoughts on this vintage and what I am planning to add to the

While Angélus appears to be too expensive (+24%) as a consequence of “a positioning strategy, combined with low quantities brought to market”, Cheval Blanc may be a bargain: released at -16% of its estimated fair value, this discount is entirely explained by the fact that this wine stands out as the great success of the vintage among the Premier Crus Classés and alike.

In other words, if its scores were closer to 95 than 98, the release price would no longer be particularly attractive, but just right.

What’s more, also Saturnalia’s Fair Price regression model suggests that Cheval Blanc was released at a 9% discount! The Saturnalia’s Fair Price is calculated using a regression model that takes into account two main hypotheses. Firstly, it correlates the Vintage Score and is computed algorithmically based on factors like vineyard position, weather data, and satellite trends, with prices.

The model assumes that wines with higher scores should have a correspondingly higher price trajectory.

Epilogue: Embracing the Fair Value Ball

As the curtains fall, investors waltz through the ballroom of fair value, empowered with insights that transcend market noise. Just as "My Fair Lady" enchanted audiences with its timeless charm, fair value captivates investors, helping them make informed choices and discover the true essence of financial success.

The million$-dollar question — is Cheval Blanc undervalued? Shall I buy some for the Saturnalia Model Portfolio?

While this fair value model does consider the previous release market prices and more generally the ˗ˏˋsupply´ˎ˗ side of the equation, it fails to account for the ˗ˏˋdemand´ˎ˗ in the context of the current economic environment. It’s not a criticism (all models are simplifications of reality) but merely an observation, and a key variable that needs to be accounted for when drawing our conclusions.

This model would probably work better in a stable/rising market — such as the one that we have experienced in the last decade; however, the current investment decisions are affected by the following:

(PS: I analyse the 🇬🇧 market, but similar conclusions can be drawn for the 🇺🇸 and 🇪🇺)

High inflation — with a rate of inflation at 8.3% and a similarly elevated figure across the traditional fine wine-hungry regions, collectors and investors are faced with the erosion of purchasing power as wage growth is still below inflation.

Raising interest rates — when interest rates are high, investors may seek other financial instruments or assets that offer (maybe) higher returns and (definitely) higher liquidity. This increases the opportunity cost of investing in fine wine, as the funds tied up in wine purchases could potentially be put to more productive use elsewhere.

Declining fine wine market prices — as discussed above, the Liv-ex 100 declining is a sign of market sentiment. It also makes it more convenient to buy back vintages than the current unbottled (and therefore, of dubious quality) wines.

In this cases, I find it very interesting to make a comparisons with the past: looking through examples of economic periods in the UK that faced high inflation and rising interest rates, we can consider the 1970s, the early 1980s, the early 1990s and the late 2000s/early 2010s. After careful analysis, the early 1990s offer the most similar market and economic environment to the current one.

📖✏️💼🏫 (history class)

In the late 1980s, the UK experienced an economic boom under the chancellorship of Nigel Lawson (the Lawson Boom). The government pursued expansionary fiscal policies, leading to a surge in consumer spending and a booming housing market. However, these policies fuelled inflationary pressures, and interest rates were raised in an attempt to control inflation. The boom ultimately led to an economic downturn in the early 1990s.

During this period spanning from 1989 to 1992, the fine wine market experienced a significant downturn. This period marked the end of a speculative boom in the late 1980s, fuelled by surging demand for investment-grade wines, particularly Bordeaux. However, the market subsequently faced a series of challenges that led to a decline in fine wine prices.

To curb inflation, the Bank of England raised interest rates sharply, reaching a peak of 15% in 1989 (hopefully we don’t get to this point!🙏). The increase in borrowing costs contributed to a subsequent period that was characterised by a slowdown in economic growth, rising unemployment rates, and, ultimately, a decrease in consumer spending — a severe recession, which lasted until 1992.

The speculative boom in the late 1980s had led to an influx of investors into the fine wine market. However, as the market became saturated, the dynamics shifted. The excessive speculation and overinflated prices became unsustainable.

The euphoria surrounding the fine wine market in the late 1980s gave way to a more cautious and skeptical sentiment. Investors became wary of the speculative nature of the market and the potential risks involved. This shift in sentiment led to a decrease in demand and subsequently impacted prices.

In addition, the introduction of the en primeur system as we know it today in Bordeaux allowed consumers to purchase wines before they were bottled, based on futures contracts. However, some châteaux adopted aggressive pricing strategies, setting high release prices for their wines. This led to a disconnect between market demand and the perceived value of the wines, resulting in lower sales and price declines.

Lastly, the outbreak of the Gulf War in 1990 created geopolitical tensions and economic uncertainties worldwide. The conflict disrupted global trade and financial markets, leading to a decline in consumer confidence and investment activities. The luxury goods sector, including fine wines, was particularly affected as international demand diminished.

Any of this sound familiar?

While the Bank of England exercises caution in its approach to interest rate hikes, it prompts us to ponder the potential impact on fine wine prices amidst similar economic circumstances.

This reinforces the skepticism surrounding the current En Primeur prices, making it difficult to believe that they are anything but excessively high.

One final comment: each wine collector and investor should arrive at their conclusion of what they believe to be a wine’s fair value. In the above, we have illustrated one way to estimate it and on Saturnalia’s platform, you can find their estimated value, which I use as a soundboard in my portfolio analysis but shouldn’t be taken as the absolute truth. The reason? They are based on mathematical models and are subject to both simplifications and a number of assumptions.

For those of you that made it till the end, what do you think? Is Cheval Blanc undervalued?

Thanks for being here! I hope you found the article rife with useful information to navigate this EP season and more generally the fine wine market.

This newsletter is free for all readers and the best way to keep it free is to subscribe, re-share it with your wine-lover friends, and follow me on Instagram.

Sara Danese

Useful Resources for Bordeaux En Primeur 2022

Lisa Perrotti-Brown, the founder of TWI, decided to make her coverage of Bordeaux En Primeur 2022 free for all 🤩 — 2022 Primeurs Early Releases and 2022 Primeurs

Colin Hay on The Drinks Business — Bordeaux 2022: ‘a miraculous and truly exceptional vintage’

Antonio Galloni on Vinous ($) — 2022 Bordeaux En Primeur: Balance Imbalance

Jane Anson ($) — En Primeur 2022: All Notes and Scoring System

William Kelley on Wine Advocate ($) — No Smoke Without Fire – En Primeur 2022

Liv-ex (free if you share e-mail address) — Critic scores, the latest Bordeaux En Primeur 2022 scores & Key prices for Bordeaux En Primeur 2022

Bordoverview (free)

I came late to the party, but this thread is worth a read (take 🍿) — Bordeaux 2022, Wine Talk

Disclaimer

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different from that of my readership. As such, the investments covered in this publication and in this article are not to be considered investment advice nor do they represent an offer to buy or sell securities or services, and should be regarded as information only.