Stop Calling En Primeur “Wine Futures”

Before En Primeur Starts, Let’s Clear This Up

Latour 2019 was released last week, and you know what that means: en primeur season is starting. Bordeaux en primeur season, that is.

This may be the shortest piece you will ever read in In the Mood for Wine: a warm-up for en primeur season, without overindulging.

Before the season starts, we need to get one thing straight. En primeur is often described as “wine futures”, including by publications that should know better. But the comparison is not exact.

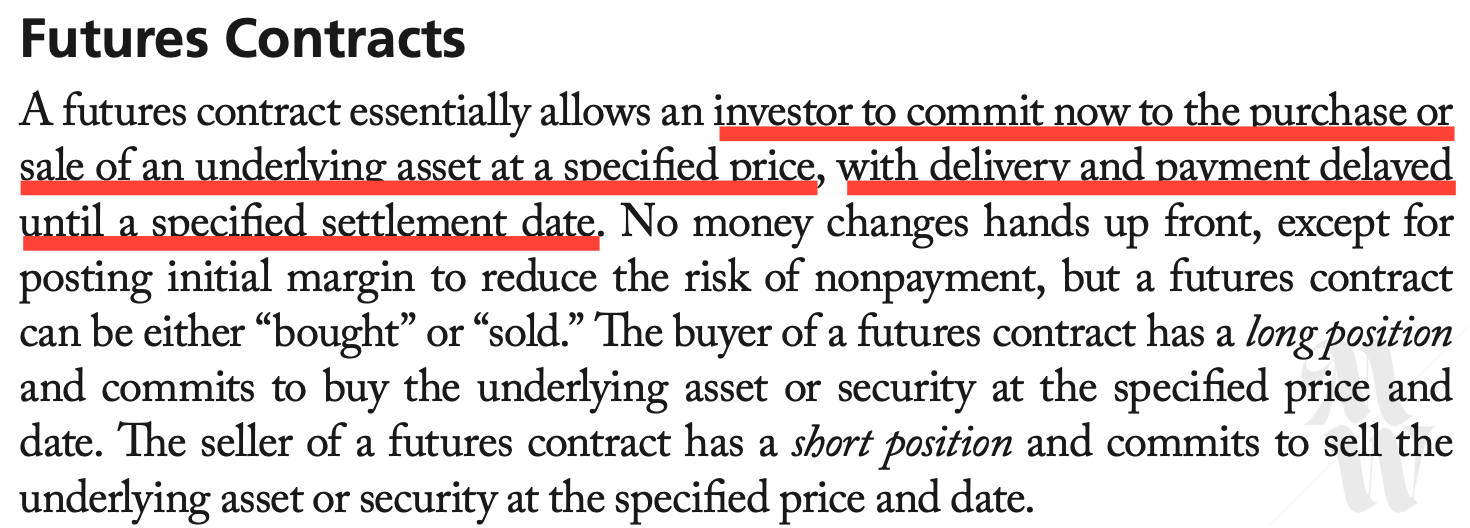

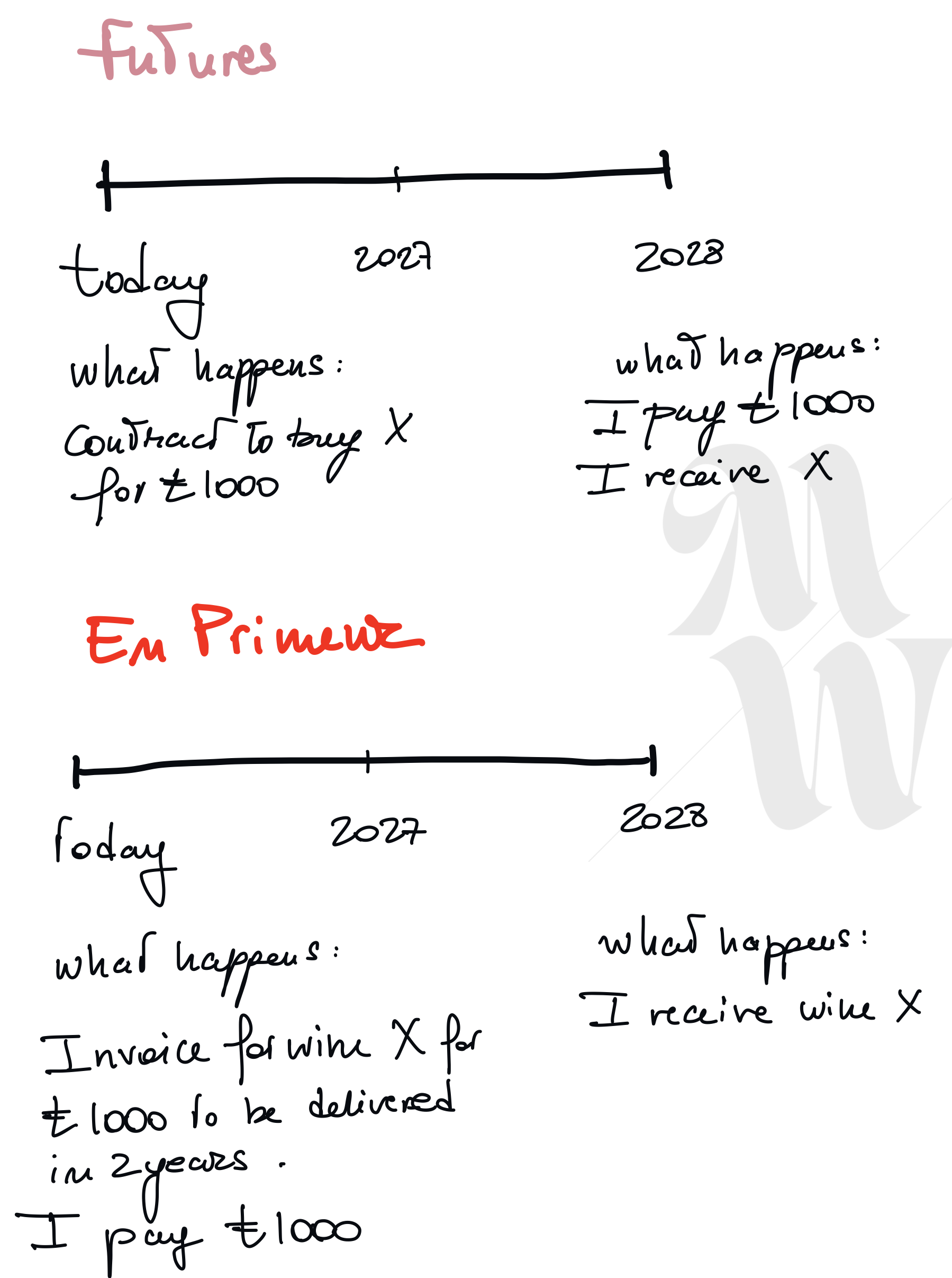

In financial markets, a futures contract is an agreement between two parties to buy or sell an asset, such as gold, at a future date for a price fixed in advance. In most cases, no cash changes hands upfront beyond a small margin, and the asset itself is not delivered when the contract is agreed.

With en primeur, by contrast, you pay now and receive the wine later.

That means your money is locked up for 18 months to two years. And whenever capital is locked up, there is a cost, whether or not you borrowed it. After all, that money could have stayed in an ISA, or been invested elsewhere, or been put to some other use.

In practical terms, this makes en primeur a very different kind of contract from a futures contract.

This is key because the structure is closer to a loan to the château than to a futures contract. And if a bank were lending that money to the château, it would want a fixed, guaranteed rate of interest over two years — say, 6% a year.

In other words, en primeur only makes sense if the buyer is compensated in some way for the risk, the wait and the lost use of capital. If not, the buyer is getting a bad deal!

Support ITMFW

This kind of analysis are unlikely to make me popular in the wine industry. If you value unvarnished, informed analysis, consider supporting In the Mood for Wine with a paid subscription or share it with someone who is tired of the usual industry lines.

Well, I’ve been buying futures ( :) sorry En Primeur) and think I get rewarded for it most times. I get wine I might find hard to get later and at a price that is cheaper than it will be later. Many times when I taste the wines I bought, I wish I had bought more from the original offer because I can’t get more or the price is much higher.

Oeno Group customers warned ‘you may not get your money back’