The Market Take

📅 Week 42

Markets in a Minute

Inflation (CPI) 12-M to September:

US +8.20% / UK +8.80% / Euro +10.00%Interest Rates (Bank Rates):

US +3.25% / UK +2.25% / Euro +1.25% S&P 500 (5D):

+4.74%Crude Oil WTI (5D):

-0.48%Gold (5D):

+0.75% CBOE Volatility Index VIX (5D):

-7.28%US$ Index DXY (5D):

-1.27%▪️What happened in the markets last week?

A lot of drama in the UK. The shortest-serving Prime Minister Liz Truss resigned. We had not one, but two (!) former Bank of England governors speaking up against the actions of this government. The latest, Lord Mervyn King, former governor of the Bank of England between 2003 and 2013, came out to say:

Markets are not in charge. Governments and central banks are. Markets respond to the announcements made by governments and central banks. And central banks have lost control of inflation, the government lost control of public finance; not surprising that markets respond to that.

He added, quite succinctly, painting a grim picture:

Public expenditure isn’t going down, if anything it will go up. Therefore taxes will have to rise to fill the gap which is there at present. That doesn’t make a very happy picture for the next few years.

The BOE had to step in, buying bonds, in an attempt to calm the markets; such action goes against the tightening policies (read: raising of bank rates) to rein in inflation. Inflation in the UK rose by 8.8% in the 12 months to September 2022, up from 8.6% in August and returning to July's recent high. On the other hand, retail sales in the UK declined in September for a second consecutive month (-1.4%), a sign that consumers are pulling back on spending.

This morning, the pound gains as Sunak leads the race to become PM.

In the US, stock markets have gained and volatility has come down, taking a respite ahead of the earning season.

Meanwhile, in China, Chairman Xi Jinping secured a third term as China’s leader after a steady drive to consolidate power. The makeup of the Politburo and Standing Committee seems to be turning away from the opening-up policies of the last two decades. As a consequence, China’s yuan weakened and the country’s stocks tumbled in Hong Kong to the lowest level since the depths of the 2008 global financial crisis, a stark rebuke of President Xi Jinping’s move to stack his leadership ranks with loyalists. More on this to come.

The Wine Market Update

(MoM = month on month)

Livex 50 (MoM):

+0.3%Livex 100 (MoM):

+1.9%Livex 1000 (MoM):

+2.1%▪️What happened in the fine wine markets last week?

Another strong week in the fine wine market. This is very surprising, especially when compared to investor sentiment, which remains at extreme bearish levels, the latest American Association of Individual Investors survey shows.

On Oct. 11, the same day the IMF warned of darker economic clouds on the horizon, the world’s biggest luxury giant LVMH posted sales that beat analyst estimates.

LVMH’s CFO Jean Jacques Guiony explains the "divorce" between global economic fundamentals-sharply rising interest rates, widespread inflation, and looming recession and the resilience of the luxury industry.

"Luxury is not a proxy for the general economy. We end up selling to affluent people and they have behaviour on their own, which is not necessarily totally aligned with economics."

LVMH may not be a proxy for the global economy but it certainly is a proxy for luxury goods. A few key takeaways that might apply to the fine wine industry as a whole:

Asia, including China, saw slower growth over the first nine months of the year, though growth accelerated in the third quarter due to the easing of Covid-19 restrictions. A recovery in China could come as consumers in the West begin to sober up from the post-pandemic euphoria.

When it comes to wine, this would translate into a continued focus on Bordeaux and Burgundy to the detriment of Italy, the US and other less established wine investment regions.

Sales at US jeweller Tiffany & Co were slowing in the US. American wealthy shoppers in Europe splashed out on making the most of the strong dollar, to the detriment of local US brands.

Transliteration of this in terms of US fine wine might be a bit behind the curve. The California 50 posted positive returns: +9.5% year-to-date, and trade hasn’t shown signs of slowing in the last month, posting gains that are only second to Champagne and Burgundy.

On another note, the thirst for Champagne seems unquenchable — and Louis Roederer’s Cristal 2014 vintage led as the most traded wine by the value this week, followed by Dom Pérignon 2012 and Jacques Selosse 2008.

Is the market for Champagne over-heated? Is the bubble about to burst? In my piece with Six Atmospheres’ Tom Hewson, we look at the market for Champagne investing:

New Wine Reports

▪️‘Full AOC Deep Dive: St Estèphe 2014 & 2016’ (janeanson.com) ($)

Jane Anson published an AOC review of St Estèphe, on the 2014 and 2016 vintages, which I very much enjoyed reading.

What an odd choice of vintages, I thought. However, Anson explains that, alongside the tasting of one of the most celebrated vintages of the past few decades, 2014 is widely seen to have over-performed specifically in the St Estèphe appellation because of low rain during summer, and a gorgeous late season that was again less disrupted by rainfall here than elsewhere. This benefitted the Cabernet Sauvignon grape in particular.

St Estèphe is the most northerly of the main four commune appellations of the Médoc and the one with the fewest 1855-classified estates: only five classed growths.

The clay in the soils is proving a boon in terms of protecting freshness in increasingly hot summers.

Jane Anson claims that “this just might be St Estèphe’s decade”

As you would expect, the 2016 is significantly riper as a whole than the 2014, and it is a vintage to buy.

Montrose was awarded 100 points for their 2016. Other top three estates — Montrose (2nd growth), Cos d'Estournel (2nd growth) and Calon Ségur (3rd growth).

A few wines to consider from the report.

Château Montrose 2014 (£85 / bottle)

2014s trade at a 40% discount of their respective 2016s. However, it feels justified as they have scored, on average, 2 pts less. If in doubt about which one to choose between Montrose 2014 and Cos d'Estournel 2014 (both second growth), the former scored 97 points (vs. 96 of Cos d'Estournel ) and is priced at a 15% discount.

[The same dynamic appears for the 2016 vintage - but the margin is much lower (<4%).]

Château Cos Labory 2016 (£21 / bottle)

I am not quite sure if Cos Labory can be viewed as a (good) investment — price of their wines in the last decade seem to be stubbornly hovering around the same £21 / bottle mark.

The one exception, their 2010 vintage seems to have doubled in price to around £40 (but is not available from UK merchants) — because a large part of the sales is direct from the château, in line with their philosophy.

However, it feels a steal for one of the (five) classed-growth estates of the appellation.

This is a definite contender for the most under-the-radar (and best value) of all 1855-classified Bordeaux, and yet it keeps quietly delivering hugely drinkable and enjoyable wines: often far less glossy than its neighbours, and one of the few classified growths to still merit the term ‘old-school’, it has stepped up gears over recent vintages.

While Anson recognises the château may lack consistency at times, she also agrees that 2016 may be the vintage to bet on.

Chateau Phelan Segur 2016 (£31 / bottle)

In Inside Bordeaux, Anson praises Phelan Segur:

This is a definite star in the appellation, and in my mind would make it into a new version of the 1855 classification in one ever came around (which it won’t!).

As you can see from the Saturnalia map, it is right next to Montrose. Phelan had expanded to 90 hectares but sold a section that was once part of Montrose back to them in 2010.

With a score of 95 points, Anson writes: “Beautiful texture and grip right from the first moment, showcasing why this is one of the best estates in the appellation.”

In addition, she praises the estate’s consistency and character.

▪️ ‘Finding value in Figeac following its promotion’ (Liv-ex)

Liv-ex reports an increased appetite for Figeac since their promotion to Premier Grand Cru Classé ‘A’ in the 2022 revision of the Saint-Émilion classification.

I will discuss Figeac in my October Portfolio Update (on 4th Nov) for my Saturnalia model portfolio, as I had added the 2019 vintage ahead of the reclassification.

▪️ ‘Not New World’ (TWI) ($)

After Catena Zapata’s landslide success, especially at the latest release on Place de Bordeaux, Argentina’s Malbecs are now viewed in a different light.

The tiny production (around 400-450 cases) of Catena Zapata Adrianna Vineyard Mundus Bacillus Terrae label has become one of the most prized and collected Malbecs, now sold via the Place de Bordeaux (since 2015) and distributed around the world. Their latest 2019 vintage was awarded 100 points by Jane Anson, and she also nominated it as her one wine to buy.

/ Twitter")

Laura Catena (the daughter of founder Nicolàs Catena Zapata and managing director of the family estate) shares the secret of their success with Lisa Perrotti-Brown in TWI: her father’s vision.

What my father started was to build around altitude. With higher altitude comes a cooler climate, slower ripening, and lower alcohols because the sugars happen at the same time as the phenolics. The big problem with this is frost. We lose out some of our crop 1 year out of 4. You just have to accept that.

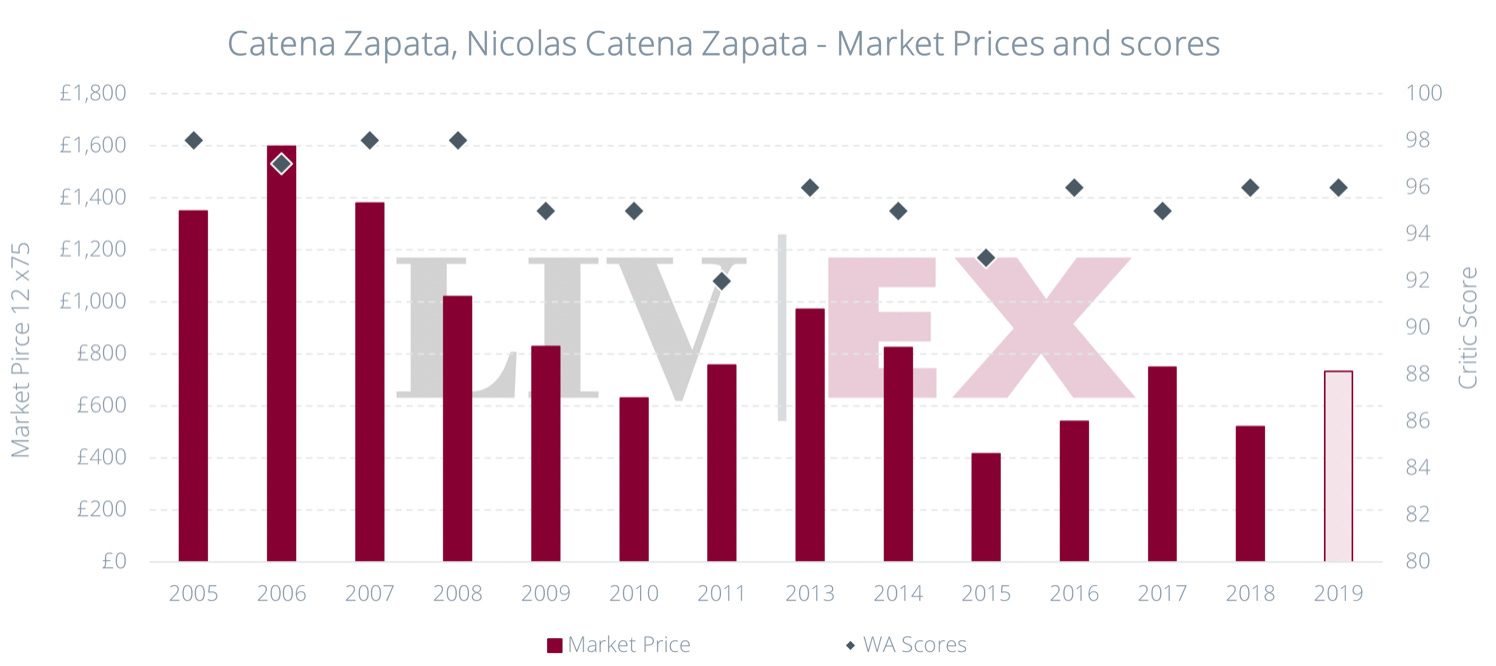

Jane Anson also believes that Catena Zapata’s 100% Malbec wines show the type of longevity we expect from very fine wines (20 years). Lisa Perrotti-Brown, in her latest article, agrees with Anson on this crucial point: tasting Nicolás Catena Zapata and Adrianna Vineyard Malbec with vintages from 1999 to 2015, she points out that the 2015 Adrianna Vineyard Mundus Bacillus Terrae “should cellar gracefully over the next 20+years.“ It scores 97 points, and currently priced at £118 / bottle, which is the most underpriced vintage (compared to £161 / bottle for the 2019).

In addition to tasting their 100% Malbec, Perrotti-Brown evaluates the Cabernet Sauvignon/Malbec blend labels (Nicolas Catena Zapata) going back to 1999. In terms of longevity, the 1999 reached its peak. “It should plateau, remaining like this for 10-12 years, before gradually fading.” The 2004 Nicolas Catena Zapata seems to even beat that, with a long life ahead lasting to 2037. Prices on the back vintages in general seem to have increased — while 2019 and other more recent ones, such as 2016 haven’t moved much since their release price.

On this note, a couple of weeks ago, I had the chance of meeting Pablo Cúneo, head winemaker at Luigi Bosca, one of the most respected and oldest Mendoza producers. I will share my thoughts on Paraíso 2019, their most prized wine and, more generally, on the new-wave Malbecs.

Private Cellar Offer

“A stunning range of Red Bordeaux, Red Burgundy and gems from Spain, Italy and the New World“ (Goedhuis & Co)