Hello wine lovers,

Are you panicking because you see offers for your wines coming through well below market price?

Don’t!

Rejoice!

The market is finally softening!

Time to pick up some bargains!

Every month, I share a report that analyses the qualitative and quantitative investment thesis of fine wines in the Saturnalia Model Portfolio built using the Saturnalia wine investment platform.

You can read the background of this project here:

Performance

During January, the Saturnalia Model Portfolio (ex-cash) lost -2.4%. During the same period, the Liv-ex 100 lost -1.4%. In relative terms, the portfolio underperformed the index by 1%.

[Please note that I calculated the portfolio return ex-cash. That’s because the ‘cash allocation’ is not strategic but is instead a £50,000 yearly budget allocated to fine wine investment, which parallels the way in which some wine collectors/investors think about their yearly allocation to fine wine.]

Attribution

Why did the Saturnalia Model Portfolio perform worse than the Liv-ex 100 in January?

For a similar reason that the Liv-ex 100 did worse than the Liv-ex 1000 —concentration.

In investment terms, concentration is the opposite of diversification. The Liv-ex 100 index is made of 100 wines, while the Liv-ex 1000 is made of (you guessed it!) 1000 wines. And the Saturnalia Model portfolio has 10.

Portfolios with a large number of positions tend to experience shallower lows — because individual positions in the portfolio account for a smaller portion of the whole.

At the same time, they don’t experience the same highs that a punchy concentrated portfolio does.

Diversification is a risk management tool, if you will. Warren Buffet said that diversification may preserve wealth but concentration builds wealth. In fact, top investors, generally, tend to adopt a concentrated investing approach, and it is this concentrated approach which empowers them to focus and invest only in their best ideas.

Wide diversification is only required when investors do not understand what they are doing.

In the world of wine collecting and investment, concentration can be a by-product of both how fine wines are released on the market and personal taste.

For example, the Saturnalia Model Portfolio is heavily concentrated in St. Emillion simply because of timing. We started this project just ahead of the 2022 St. Emillion reclassification and it was important to capture the potential upside of upgrades. More generally, whenever a vintage from a certain region is released, buyers ‘bulk buy‘ from that release, leading to unwanted concentration.

Wine collecting isn’t just an investment such as buying shares in Apple — it has a hedonistic side too. In the last edition, we discussed the importance of diversifying away from strictly what we like at the moment to factor in that a palate will evolve over time.

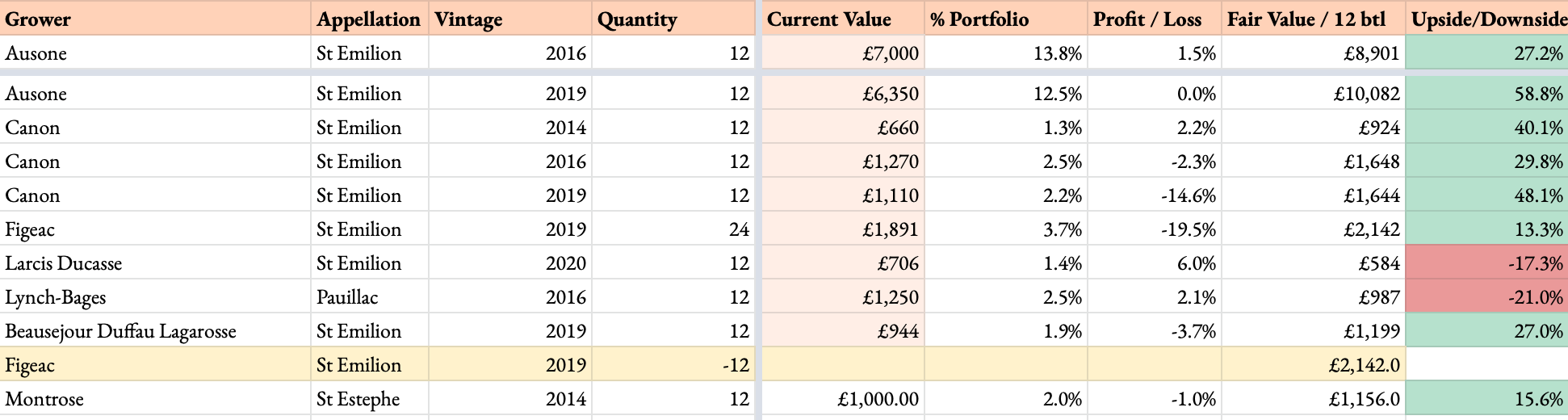

While concentration may be an unwanted side effect of wine investing, the more important question to answer is whether the portfolio behaves as we would expect it would. In the case of the Saturnalia Model Portfolio, the 10 positions faced a negative downturn in line with the trend of the wider market in January. However, because of concentration, two positions, Figeac ‘19 & Canon ‘19, were responsible for the majority of the losses.

The three major movements that impacted the portfolio were:

Figeac 2019 ↓

Figeac was by far the biggest contributor to the portfolio losses. Just in the month of January, Figeac 2019 lost -19.5% and -25.8% from its highs in October, when I sold it at £2,550 / 12 bottle case.

(60% of my readers told me not to do this, I wonder if they still think it was a crazy idea? 😜)

In addition, the concentration of the portfolio comes with a regional bias, as all 10 positions are within Bordeaux and most of them are St. Emillion bets. This means that the portfolio has systemic risk, i.e. the risk that derives from the market and not a position itself, especially when compared with a broader index.

St. Emillion, as a region, performed well following the reclassification. And because of it, it can be expected to be more impacted by a market downturn.

Canon 2019 ↓

We are experiencing a similar dynamic for Canon 2019 as we have for the Figeac from the same vintage.

Indeed 2019 seems to have been hit pretty hard in general. If we take a look at the first growth index Liv-Ex 50 (which includes the latest 10 vintages of each châteaux), we can see that among the worst performers for January we can find four 2019s. Why?

My guess is that as 2019 came out in bottle a year ago and received widely positive reviews, in contrast with disappointing En Primeur 2020 and 2021 campaigns. The release price was also more competitive than 2020 and 2021 vintages — allowing for a surge in demand for 2019s in the last couple of years.

In terms of vintage diversification, however, this is broadly what I want to have in my portfolio: mostly on-vintages and some smaller positions on off-vintages. That’s because vintage quality drives long-term appreciation.

Portfolio Changes

Finally, the market started to soften — which means it may be time to pick up some wines here and there.

First — Figeac & Beausejour Duffau Lagarosse are on my priority list as potential buys.

At this point, the Saturnalia Fair Value model shows incredible upsides from the latest prices to their model “fair value“, especially when it comes to 2019 vintages: Ausone 60%, Canon 48%, Beausejour Duffau Lagarosse 30% and Figeac 13%.

Although Ausone shows a larger potential upside, I am not considering it as a potential buy, because of the already sizeable position in the portfolio.

The same for Canon.

I am cautiously waiting to see what Figeac and Beausejour Duffau Lagarosse will do in the next couple of months to see if prices will free-fall or hold out.

What about you? Have you panicked or picked up any gems? Let me know in the comments or privately…

Best,

Directory of All Investment Cases

New? Sign Up Here

Got Feedback? Just Hit Reply

IG: In the mood for wine

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different from that of my readership. As such, the investments covered in this publication and in this article are not to be considered investment advice nor do they represent an offer to buy or sell securities or services, and should be regarded as information only.