The Price of Wine [From the Archive - Now With Voiceover 🎙️]

What are the drivers of fine wine prices?

Good morning wine lovers,

Today’s WineLeaks is slightly different — we will dive into an academic paper to discover what are the main drivers of fine wine. I hope that will help you make future collecting/investing decisions.

The Wine Market Update

(MoM = month on month)

Livex 50 (MoM):

-1.1%

Value 404.66Livex 100 (MoM):

-0.4%

Value 420.51Livex 1000 (MoM):

-0.6%

Value 482.15 What happened in the fine wine markets last week?

▪️The Liv-ex 100 dipped 0.4% in November, for the second month in a row. This downward trend started during the summer but halted in September thanks to the sterling weakness.

▪️In the November Model Portfolio update, published last Friday, I dive into the performance of Figeac 2019 & Ausone 2016 — the two biggest movers of the month.

The Price of Wine

What are the drivers of fine wine prices?

Written by Dimson (Cambridge Judge Business School & London Business School) Rousseau (Vanderbilt University) and Spaenjers (HEC Paris), The Price of Wine is considered one of the most convincing investigations into the returns of fine wine.

That is because of the data used: a long time series, with sales data from 1900 to 2012 from Berry Bros. & Rudd and Christie’s London.

In order to do that, only the five First Growth (namely, Haut-Brion, Lafite-Rothschild, Latour, Margaux, and Mouton-Rothschild) were included as part of this analysis. The reasons have to do with the availability of sales data. The first growths were sold under the château’s name (not under the merchant who had imported it) and can be traced back to 1788.

[Real returns are lower than nominal returns, which do not subtract taxes and inflation.]

The results

The annualised real financial return of wine investment (net of storage & insurance) is 4.1%. This exceeds other collectables such as art and stamps as well as bonds. However, equities have offered better returns than fine wine, especially on shorter horizons.

The article doesn’t mention which one is the best-performing asset class in risk-adjusted terms.

The quality of the vintage

In the very first article on In the mood for wine, titled Can wines from bad vintages be good investments?, we explored this point exactly.

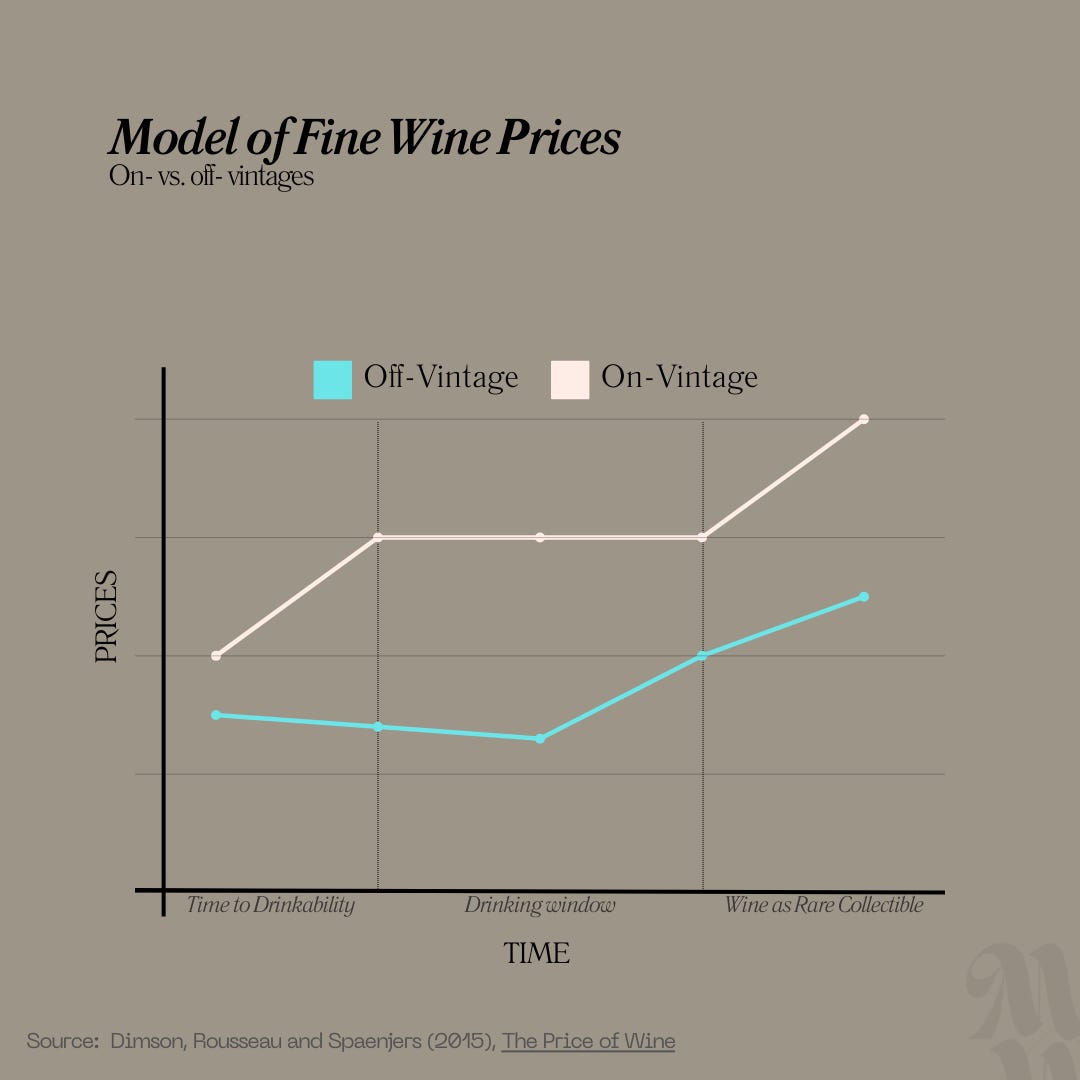

What’s clear from this paper is that, as simplified in the chart below, wines from low- and high-quality vintages exhibit very different life-cycle patterns.

Young maturing wines from high-quality vintages are shown to provide the highest financial returns.

The biggest difference between on- and off-vintages has to do with the so-called ‘consumption value’:

The consumption value of off-vintages declines quickly after bottling, as the wine doesn’t benefit from ageing.

The consumption value of on-vintages improves after bottling and rises strongly until maturity and then stabilises. Eventually, as these wines begin to be regarded as collectables (instead of consumption goods), prices advance again.

Another interesting effect is that of ageing on prices and returns. Even wines that have lost their gastronomic appeal (after their drinking window) can be valuable if it provides enjoyment and pride to their owner, thus increasing their value. A similar non-financial utility can be observed when investing in socially-responsible mutual funds or ESG portfolios.

Why do off-vintages start increasing in value eventually?

The hypothesis advanced by the authors is that off-vintages lose their consumption value more quickly. As they are more likely to be consumed when still young, we should expect that the trading volume of these wines goes down more rapidly, offering evidence that they become rare.

Storage & Insurance costs

Storage is key to preserving the condition of a bottle of wine through the decades — so much so that wines with questionable provenance are less likely to be sold by auction houses.

Storage costs have significantly decreased through the years, representing a 0.94% of the average price for 12 bottles in 1940 to 0.23% in 2000.

A typical wine insurance contract costs 0.5% of the market value of the collection per year.

Over the period analysed by the authors (1900 to 2012), storage and insurance account for an annualised rate of 1.2%.

Booms and busts

Wine prices didn’t increase in real terms in the first quarter of the 20th century — but boomed during the Second World War (+600% between 1940 and 1945). It was followed by a sharp decline after the war.

From 1950, the price of wine grew strongly although they were punctuated by declines of 20% or more in 1973-1975, 1980, 1990-1992, 2003 and 2011-2012.

Wine and Wealth

Wine is intrinsically tied to financial wealth, which reflects the discretionary nature of luxury goods. Thus, the price appreciation of wines over time is determined by the growth of wealth.

Sometimes I hear that fine wine investors are so wealthy that they are unaffected by economic cycles. That may be true in certain pockets of the market — but for fine wine prices to appreciate, they are intrinsically tied to economic cycles and growth in wealth.

Wine and Other Asset Classes

This paper found that fine wine returns exceed those of other collectables such as art and stamps as well as bonds.

In addition, future returns of wine can be predicted to be lower after periods of outperformance relative to other collectables.

In the last two years, fine wine returned 37% which is much higher than diamonds, art and other collectables.

Equities have offered better returns than fine wine, especially on shorter horizons. What’s more interesting is that returns of equities and wine are positively correlated. That goes back to wealth. As wealth is tied in the equity market, during periods of market buoyancy, wealth will increase, which in turn drives fine wine prices upwards.

Conclusions

I believe this paper can offer some powerful tools and insights for wine collectors & investors.

Here are my top 5 takeaways:

The macroeconomic environment matters. The paper clearly highlights how the price of fine wine is intrinsically linked to wealth growth and is correlated to the performance of equities. Analysing the movement and sentiment of the markets can offer insights into the trends of fine wines.

Beware of unrealistic returns. The fine wine market has just experienced a strong two-year performance and comparisons have been drawn with the returns of the S&P 500 (e.g. “Livex 100 outperforms S&P 500”). This paper however clearly shows that investing in the stock market offers higher returns on average. Therefore the recent buoyancy of the fine wine market, especially when compared to that of equities, highlights a displacement and should be treated with caution.

Vintage matters. The paper analyses the five first growths, which have an established reputation and a strong brand to support them. That’s why this analysis is so interesting — we can understand the behaviour of the vintage effect, without the interference of the brand or other effects.

Release price matters. The 2020 vintage (an off-vintage) en primeur release prices were much higher than the 2019’s (an on-vintage). What would the effect be on future prices?

A sharper drop in the 2020 consumption value? Or the levels of the 2020 prices will continue to be higher than 2019 because of the difference in release prices? I believe with two such close vintages, we can expect the former, but that’s just my opinion.

For drinking or ageing? Off-vintage wines aren’t for the bin. I’ve tasted very interesting off-vintages that have incredible aromatic profiles, and are incredible wines to drink within a few years of their release. However, they are less likely to stand the test of time. Conversely, on-vintages may be fantastic in twenty years — and may offer some decent returns. A great portfolio management tip from Jamie Ritchie, Worldwide Head of Wine for Sotheby’s (which I’ll delve more into next week) is to divide wines into every-day, special occasions and rare occasions and schedule the consumption based on the lifespan of the wines available.

I hope you found this useful. If you did, why not share it?

Thank you!

Sara Danese

Directory of All Investment Cases

New? Sign Up Here

Got Feedback? Just Hit Reply

IG: In the mood for wine

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and significantly different from those of my readership. As such, the investments covered in this publication and in this article are not to be considered investment advice nor do they represent an offer to buy or sell securities or services and should be regarded as information only.