Good Morning Wine Investors,

You might have noticed that no WineLeaks was published this week —sorry, I was in Sicily trying some delicious wines from Sicilia DOC. It will be back on schedule next Monday.

Each first Thursday of the month, I share a report that analyses the qualitative and quantitative investment thesis of the fine wines in the model portfolio built using the Saturnalia platform. You can read the background of this project here:

If you are new, join here to receive straight to your inbox updates about this project, WineLeaks, a curated overview of the wine market, and other in-depth reports.

Performance

During November, the Saturnalia Model Portfolio (ex-cash) returned 0.4%. During the same period, the Liv-ex 100 lost -0.4%.

[Please note that I calculated the portfolio return ex-cash. That’s because the ‘cash allocation’ is not strategic but it’s a £50,000 yearly budget allocated to fine wine investing, perhaps in the same way that some wine collectors/investors think about their yearly allocation to fine wine.]

Attribution

The three major movements that impacted the portfolio were:

Figeac 2019 ↓

Last month, following a stellar performance of Figeac since its promotion to 1er GCC A, I decided to unwind 50% of the position (a 12-bottle case). Figeac went from £141 / bottle to £212.5 / bottle (+50.7%) in a matter of weeks, which prompted me to review my position.

That was because of two reasons. First, I wanted to lock in some profits. And secondly, because of Angelus’ and Pavie’s price gains in the three years following their upgrade in 2012. On average, they gained 42% and 23% respectively. That was tiny if compared to Figeac's 50% jump in price over a few weeks.

Figeac 2019 lost 5.9% in November, as the fine wine market as a whole turned more cautious.

Should have I sold more? In my view, no. It was a prudent decision to lock in some of the gains, but a long-term view favours Figeac 2019. Especially, when accounting for a streak of disappointing vintages thereafter (not specifically Figeac’s): 2020, 2021 and in all probability, 2022.

On this note, Saturnalia will release a vintage report on the 2022 vintage, which, let me tell you, will not enthuse anybody.

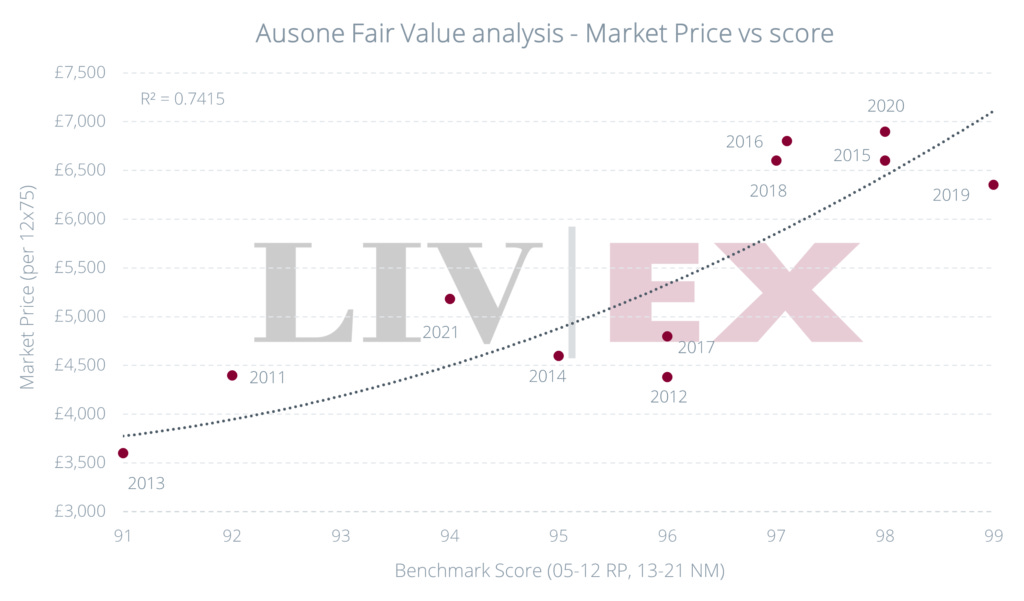

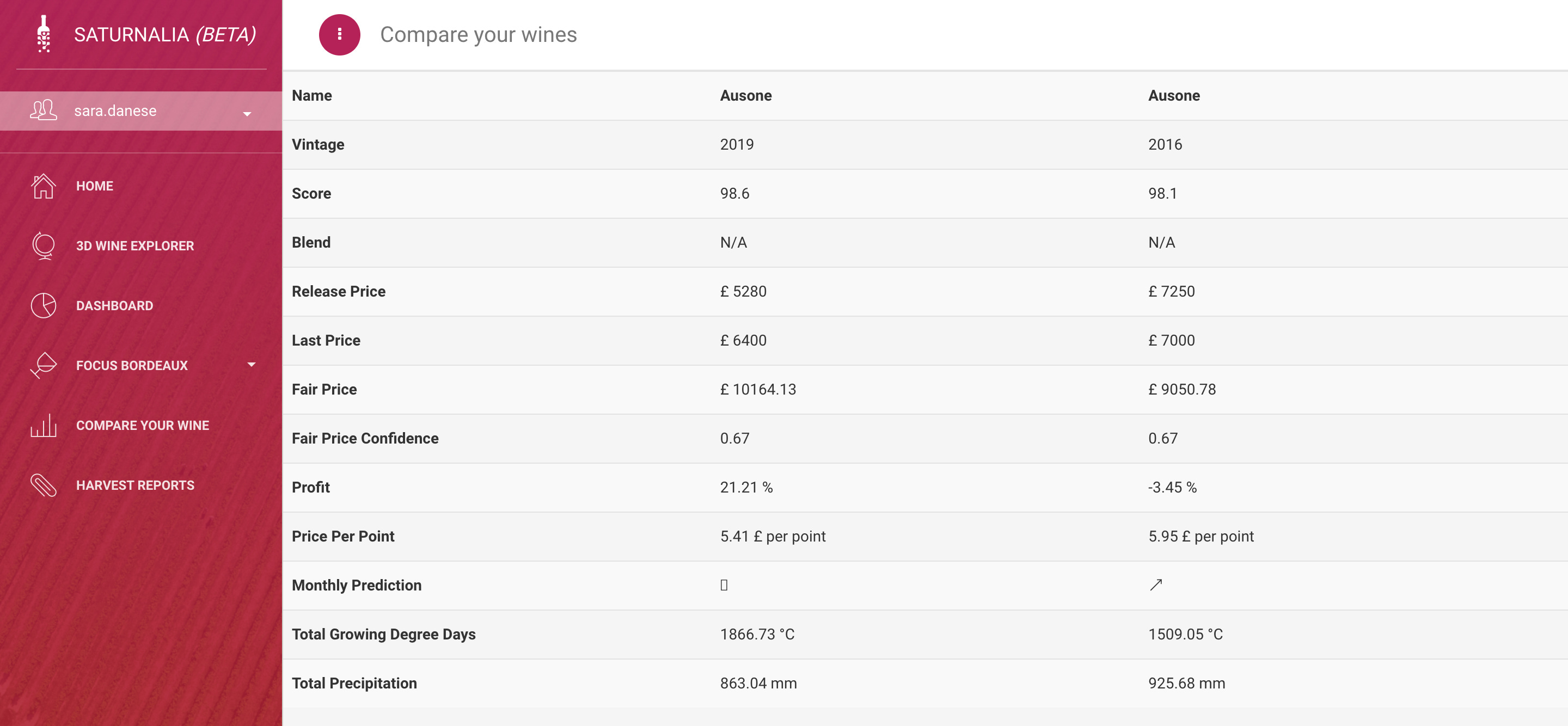

Ausone 2016 ↑

In early November, Liv-ex published a report on Ausone, confirming our view on its great value, both compared to peers and in terms of fair value.

On the Right Bank, in the last three years, Ausone underperformed both its St-Emilion’s neighbours (Château Angélus, Château Pavie and Château Cheval Blanc) as well as Pomerol’s superstars (Petrus, Le Pin, Lafleur).

In terms of Fair Value, the Liv-ex method shows that while 2019 is wildly underpriced, the 2016 seems to be overpriced. By Saturnalia’s analysis, on the other hand, both vintages are still underpriced (by 59% the 2019 and by 29% the 2016).

The difference is in the average critic’s scores.

Liv-ex’s average score for the 2016 vintage seems rather low — especially considering the major critics scored it all well-above 97: Decanter 99, Neal Martin 98-100, Jancis Robinson 18+, Wine Advocate 99. It’s fair to say that Saturnalia’s average score of 98.1 (2016) more accurately reflects the average score of most wine critics.

Perhaps because of this Liv-ex coverage, the Ausone 2016 increased in value during November, which was the major driver of positive performance for the portfolio this month.

Other wines ↓

Generally, the market trend for November was downward — certainly for Bordeaux. All the other names in the portfolio were pulled down by such market forces.

Portfolio Changes

During November, I explored the Bordeaux 2020 vintage, following a tasting at the Union des Grand Cru de Bordeaux. 2020 turned out to be a complicated vintage (favouring the Right Bank) and, more importantly, an expensive one!

Taking as an example Trotanoy, one of my favourite wines of the vintage: their 2020 vintage is selling for £311, while 2019 is for £253.

While Trotanoy 2020 was awarded some incredible scores, it’s important to consider the supply-demand rationale here. 2020 was a vintage that somewhat disappointed everywhere else and some, generally Right Bank, names stood out. Critics awarded the best scores and buyers jumped on them, inflating the 2020 (already high) prices even higher. Another similar example of this phenomenon was Canon.

2020 is a tough sell — and, because of this, probably one of the least traded vintages in Bordeaux.

In addition, my current portfolio allocation is skewed towards the Right Bank, except for Lynch-Bages (2.4% of the portfolio).

Looking elsewhere, you may remember the deep dive in St Estèphe 2014 & 2016, following Jane Anson’s report. In the report, it turned out that, while 2014 is considered an ‘off-vintage‘, it is widely seen to have over-performed specifically in the St Estèphe appellation because of low rain during summer, and a gorgeous late season that was again less disrupted by rainfall here than elsewhere. These conditions benefitted the Cabernet Sauvignon grape in particular.

Among most of the names, Montrose stands out, for a few reasons:

2014 is an off-vintage that might be offering some hidden value because it is still considered the best among off-vintages and because St Estèphe 2014 overperformed.

Montrose 2014 trades at a 40% discount from Cos d'Estournel 2014. They are both second growth and both have very similar critics’ scores.

Montrose 2016, however, doesn't seem to trade at a significant discount from Cos d'Estournel 2016 — highlighting that the gap isn’t normally that wide.

Saturnalia’s fair price model shows Montrose 2014 to be undervalued.

In light of this, I’ve added 12 bottles of Montrose 2014 to the portfolio.

I’d love to hear your thoughts in the comments!

Best,

Sara Danese

Directory of All Investment Cases

New? Sign Up Here

Got Feedback? Just Hit Reply

IG: In the mood for wine

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different from that of my readership. As such, the investments covered in this publication and in this article are not to be considered investment advice nor do they represent an offer to buy or sell securities or services, and should be regarded as information only.