Sterling, Dollar, Euro: How Currencies Shape Fine Wine Prices & Trade

A short discussion of currencies in wine

If all the wine in the world was produced on the ficticious island of Lilliput and all the inputs to make the wine were to be found on this island and all the buyers of said wine lived on the island and wine and raw materials and workers could be paid in the local currency “sprug,” then currency wouldn’t have any effect on the price of wine.

Alas, wine isn’t made in an insulated bubble.

Precisely because it’s tied to place (you can’t make Champagne in Minnesota), it’s a heavily traded, export-driven product. And yet it can be both economically marginal and politically useful, a token weapon in trade wars. For example, China’s ban on Australian wine, and more recently President Trump’s threat of 200% tariffs on Champagne. It’s marginal because, in the grand scheme of a nation’s economy, wine isn’t essential to the basic functioning of the state. But it’s also significant: for France, wine and spirits are the country’s third largest export category, which is precisely why wine so often becomes a convenient PR/social media pressure point in disputes.

Which is to say: trade, and consequently, currency moves affect the cost of wine. A lot.

Italy, France and Spain are the world’s three largest wine producers. Together, they account for roughly half of global output — and the picture is even more skewed towards Europe when you look at “fine wine”. (Putting a precise percentage on that is impossible, because there’s no agreed definition of what fine wine actually is.)

When wine is made in Europe, most inputs are priced in euros — labour, electricity, glass, paper and cork — which means wine, and especially fine wine, is largely a EUR-denominated asset. Producers typically quote an ex-cellar price in euros to merchants. Importers then buy in euros and also pay for insurance and shipping, often in euros as well.

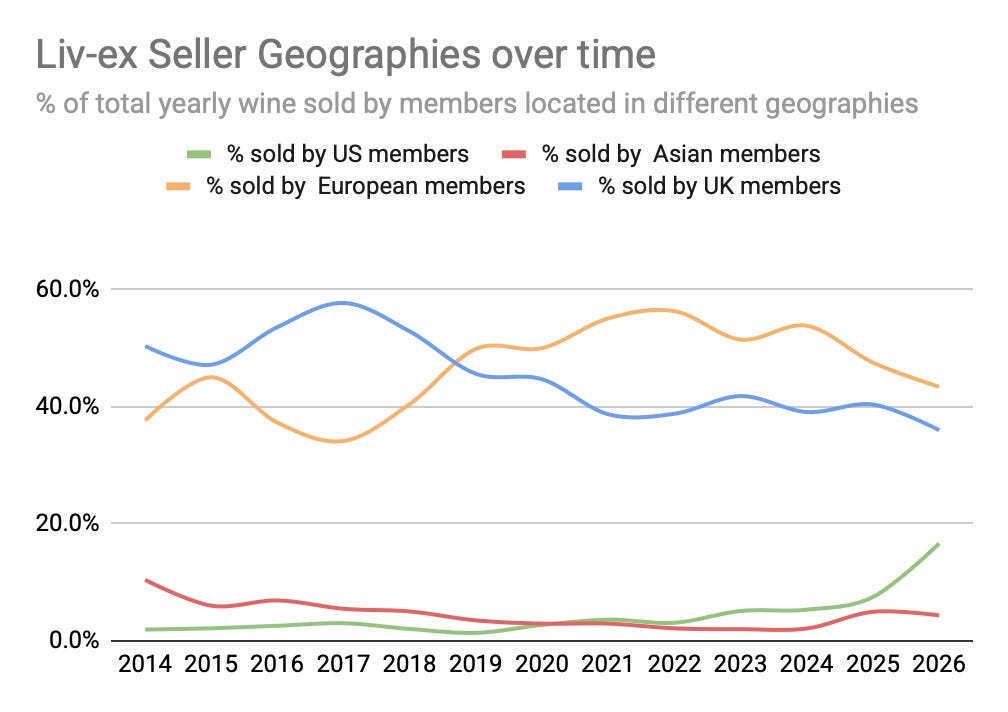

Once it reaches the secondary market, fine wine remains, for the most part, a EUR asset — but it tends to also be quoted and traded in GBP. That said, as you can see from the Liv-ex chart below, trading is still largely driven by European players (around 45%) and UK players (around 40%).

That’s why currency moves have a significant impact on the price of wine — and, perhaps even more importantly, on trading activity and volumes.

Brexit & the Sterling

The impact of a weaker GBP (as we experienced around Brexit) is a very practical example of the impact currency has on the price of wine.

If UK buyers suddenly have less purchasing power — about 20% less, in that episode — you would expect trading volumes to fall. A wine that previously cost a UK buyer £100 now costs £120, purely because the local currency has weakened.

And yet, during the same period, the Liv-ex indices were pointing to a rally in fine wine prices.

Why?

First, the Liv-ex indices are widely seen as a bellwether for the fine wine market.

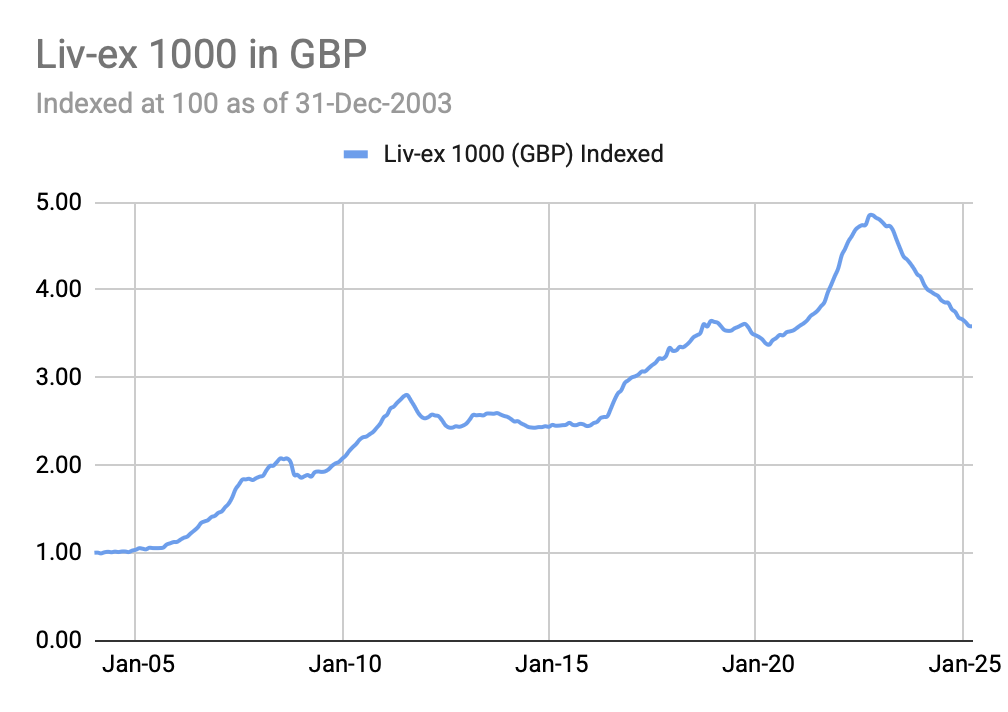

And because Liv-ex is based in London, its indices are quoted in GBP. Over the past 20 years, the main Liv-ex index has risen by roughly 3.6x.

However, the currency you look at matters.

The chart above is effectively saying: if you’re a UK-based (GBP-based) merchant or collector holding mostly European wine assets, the value of those assets has increased roughly 3.6x over the past 20 years in GBP terms.

But how much of that is a true increase in the underlying wine price, and how much is simply a currency effect?

A simple way to think about it is:

GBP return ≈ EUR return + change in EUR/GBP

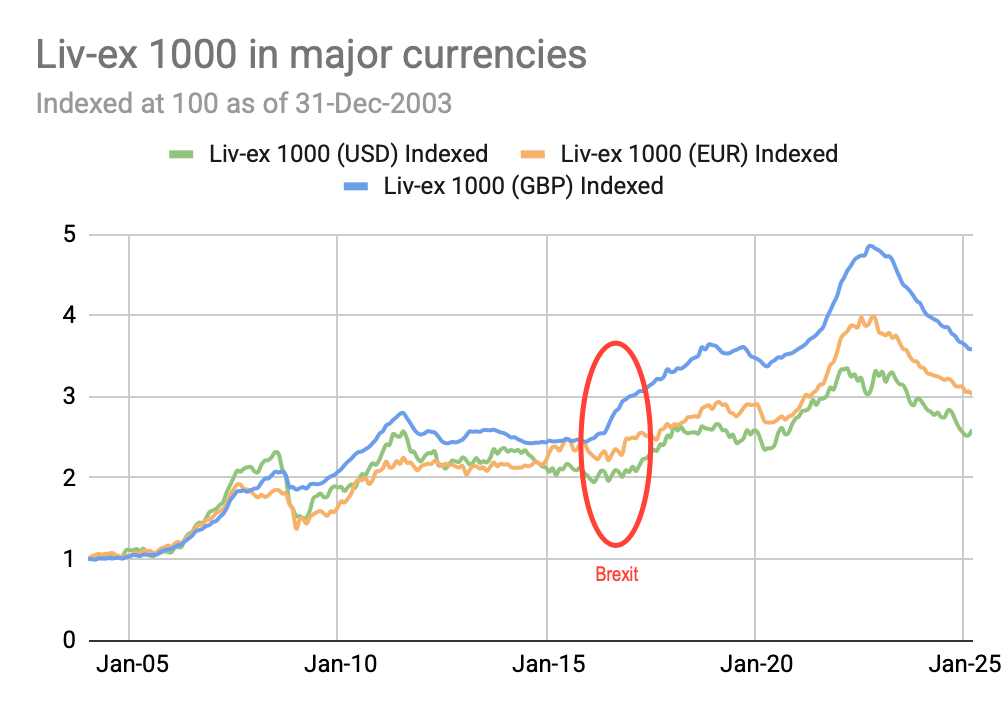

Investors often underestimate the currency component because it’s “baked into” the total return. It becomes painfully obvious during large dislocations — Brexit being a good example. If you take the same index and convert it into EUR (and USD), the picture can look very different, as the chart below shows.

Over the same 20-year period, that very same index returned roughly 3x in EUR and 2.6x in USD. In other words, a meaningful part of the 3.6x headline return in GBP wasn’t “wine performance” at all — it was GBP weakening.

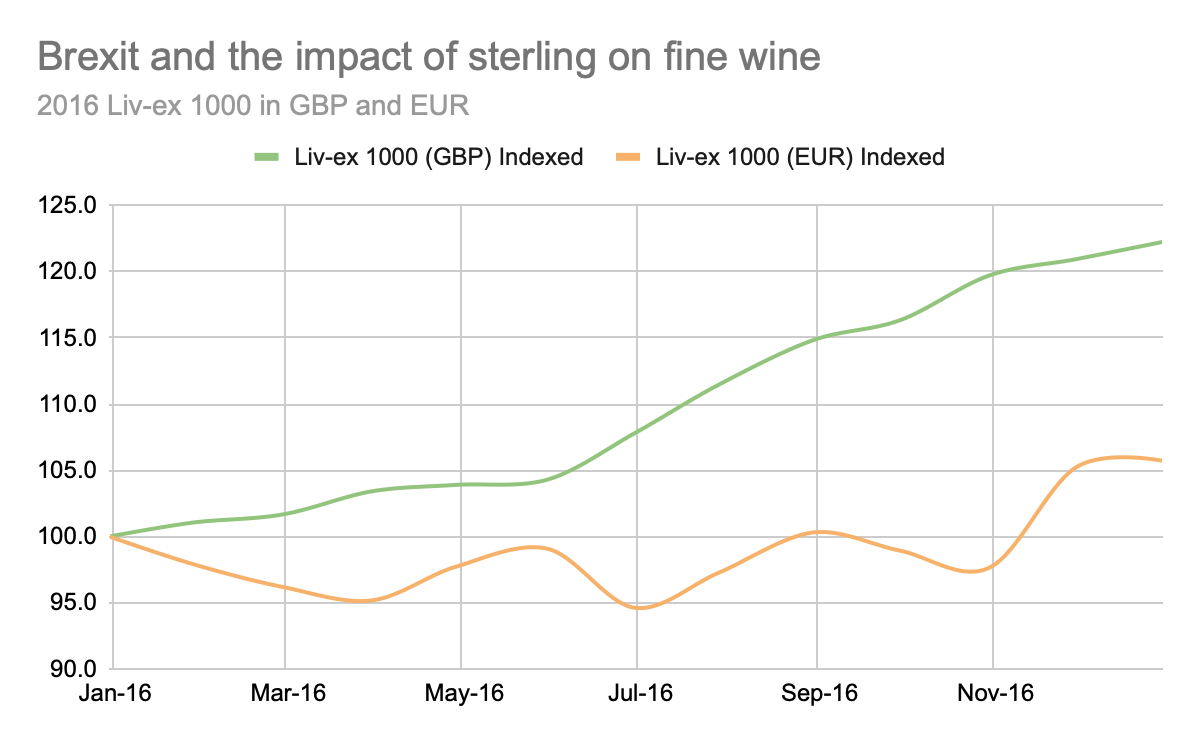

If we zoom in on that period, the mechanics become clearer:

In 2016, the Liv-ex 1000 index was up 22% in GBP, while the same index was up only 5% in EUR. The gap (around 17 percentage points) was largely driven by the sharp move in sterling.

What does it mean?

That means that, in 2016, if you were a GBP earner holding European wine, you were effectively short sterling and long euros. Your asset would have appeared to appreciate by 22% in GBP terms — roughly 5% from the underlying move in wine prices, and about 17% from the depreciation of the currency you were “short”.

If, on the other hand, you were a EUR or USD earner holding European wine, you would have captured the c.5% move in the wine market, but little (or nothing) from that GBP currency effect.

You may, of course, have had other currency exposures depending on where you bought, stored, and sold — but the broader point stands: understanding your currency exposure is crucial, especially in periods of trade instability.

A disclaimer: of course, the interaction between currencies and wine prices isn’t this clean. As the charts above show, it’s not just two currencies at play. The effects are more complex — especially in wine, which trades globally and moves between multiple currency zones.

Ten years on, we can take the lesson from sterling and apply it to the US dollar — the currency currently experiencing the most instability.

Tariffs & the US Dollar

President Trump wants a weak dollar. President Trump wants a strong dollar. President Trump wants tariffs. President Trump wants low interest rates.

A weaker US dollar can help exports, but a stronger dollar helps preserve its status as the world’s reserve currency. Tariffs can, in theory, support the dollar by reducing demand for imports. Lower rates can do the opposite by making dollar assets less attractive.

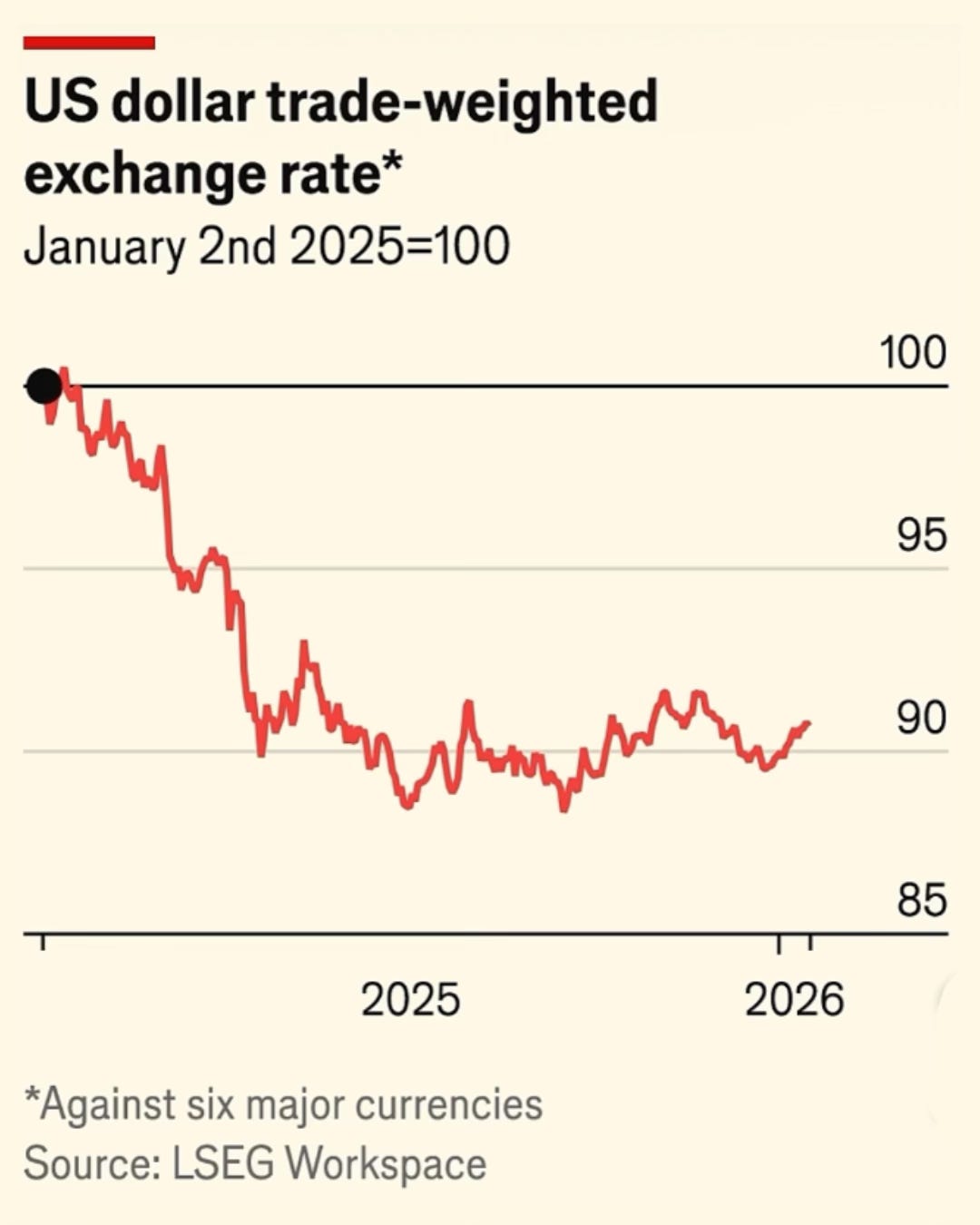

What matters, though, is what markets are doing. Since Trump first announced the tariffs, the US dollar has weakened by roughly 10%.

In Trump’s America, two developments have already had clear implications for wine: tariffs and a weaker US dollar.

These two phenomena are linked. Standard economic theory suggests that an import tariff should put upward pressure on the tariff-imposing country’s currency (US dollar): tariffs tend to appreciate the home currency, offsetting part of the tariff’s effect on import prices. In other words, if a 15% import tariff is applied to imported wine, a stronger dollar should make that tariff less painful in dollar terms.

But that is not what happened.

Since the tariff announcement, the dollar has weakened by around 10% against a basket of major currencies. One interpretation is that foreign investors reduced exposure to US dollar-denominated assets, selling dollars and rebalancing towards other major currencies.

This means the tariffs (and, arguably, the instability and uncertainty around them) have delivered a double whammy: they have pushed up the sticker price of imported goods by 15%, while the weaker dollar has made those same goods roughly 10% more expensive again for US buyers. Taken together, the effect is not strictly additive, but the direction is clear: US buyers are facing a materially higher all-in cost for imported wine.

Enter VOS Selections:

Victor Owen Schwartz, a small New York City wine importer, and his supporters took on President Trump over tariffs, first at the Court of International Trade, and then at the Supreme Court. Their argument was that Trump’s broad “emergency” tariffs under IEEPA did not extend to taxing imports. The law was designed to enable financial and other sanctions against states such as Iran and North Korea; it never mentions tariffs.

VOS won unanimously at the Court of International Trade, a federal court that hears civil cases linked to customs and trade laws. It then won again on appeal. On Friday 20 February, it sealed its victory with a decisive Supreme Court judgment.

When asked why he decided to take on the President of the United States over tariffs, what came through was a painful reminder of how vulnerable the wine sector is to geopolitical decisions — and what ultimately pushed Victor Owen Schwartz to take a decision that could have cost him everything. As he put it: “what kept me up at night was my business. Running a business kept me up at night more than this case.”

What VOS Selections did is to rein in unchecked discretionary authority — specifically, limiting a president’s ability to impose tariffs on a whim simply by declaring a national emergency.

Who doesn’t love a David-and-Goliath story? This victory, however significant, brings fresh uncertainty back into global trade — and uncertainty is what tends to freeze activity.

That’s why I don’t think it’s a victory for the wine industry just yet. As of today, Monday 2nd March, Trump is imposing new tariffs of 15%.

A 15% tariff, coupled with a roughly 10% devaluation of the US dollar against the euro and sterling, plus the renewed uncertainty, suggests we could see demand for fine wine weaken again.

That may well act as a headwind to the “green shoots” many industry outlets have been reporting.

Final Thought

That is why, precisely because wine is so exposed to trade policy and geopolitical risk, I would caution against arguments that present it as a scarce store of value or a hedge against political shocks, based solely on the historical performance of Liv-ex indices.

Because of their structure, an euro asset quoted in sterling can look as though it is rallying during periods of particular sterling weakness against the euro. Taken at face value, that can be mistaken for “wine going up”, when in reality much of the move is simply currency translation.

Anyone who imports or exports wine knows this instinctively. In periods of political instability and currency stress, wine does not behave like a safe haven. It is a highly illiquid, risky asset traded in a largely unregulated environment, with wide bid-offer spreads — the exact opposite of what most investors want to be holding when markets turn frantic.

You should also read this article from one year ago:

Welcome To A Safe Haven

When I wrote Is Fine Wine Really an Inflation Hedge?, I received a few comments from people in the industry that went something like this:

“Nice analysis, but just not the kind of messaging we’d use to sell wine.”

This is exactly why In the Mood for Wine exists: a safe haven from the unsubstantiated claims that swirl around the wine industry—often just so that “they can sell more wine.”

I have no issue with disagreement. I welcome it. This is a free world, and different perspectives and interpretations of the big data are not only allowed—they’re essential.

I believe deeply in the Socratic method.

What I do take issue with is the disingenuous—and often ignorant—way wine is sold. It’s why the moment I mention “wine investment,” people start telling me stories of how they were scammed.

Support ITMFW

Love In the Mood for Wine? A paid subscription helps keep the free edition accessible to everyone — and unlocks exclusive perks for you. Or, you can simply share this article and the newsletter to help grow the community!