The simple framework I use to judge EP pricing (Part II)

Are this year’s release prices actually fair so far?

A few weeks back, I published “The simple framework I use to judge EP pricing”rather hastily, following the release of Pontet-Canet. Before sharing more conclusions, a few clarifications are in order.

Starting with the language. Much of what is said around En Primeur pricing sounds precise but is, in fact, meaningless. “Released at a 5% discount to last year.” “10% below the 2019 market price.”

These statements don’t mean anything.

They are comparing apples with pears. If you compare today’s release price with the market price of back vintages without adjusting those back vintages for the cost of carry, then you are comparing two fundamentally different things.

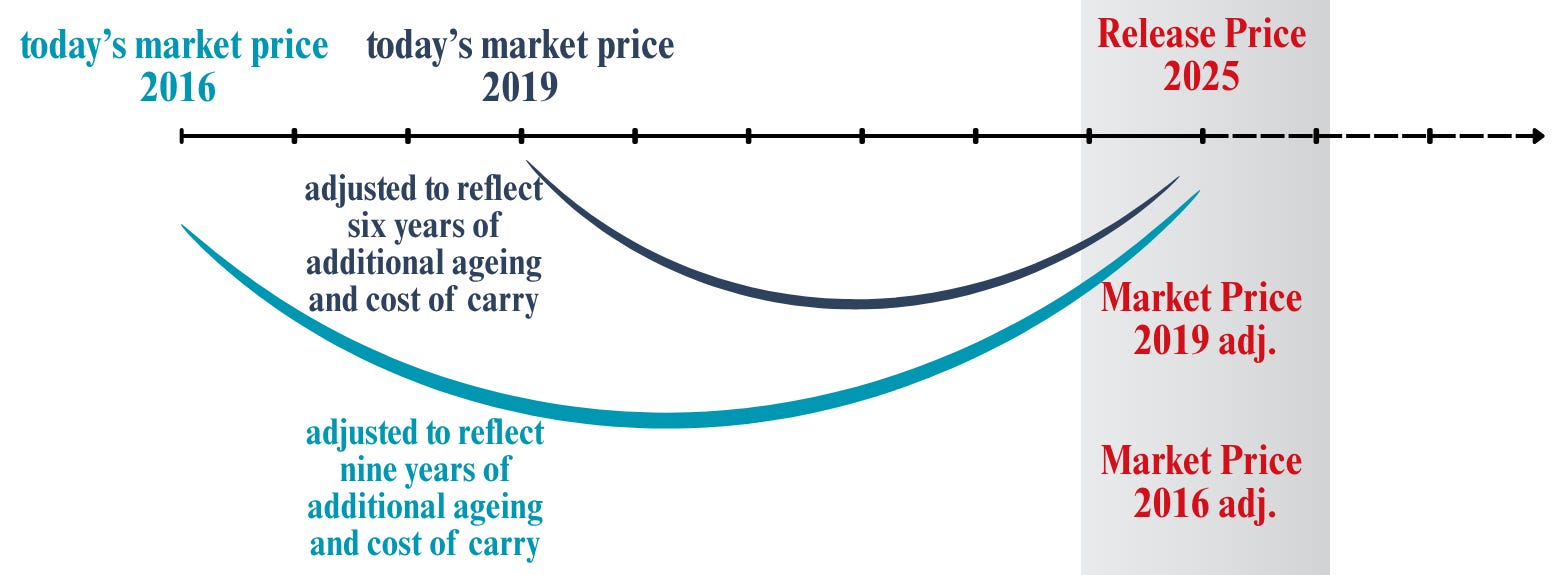

Today’s market for back vintages matters when evaluating current EP prices but to arrive at some reasonable measure of release value for this campaign, I took the current market prices of recent benchmark vintages — primarily 2016 and 2019 — and adjusted them to reflect the additional ageing time those wines already possess relative to the newly released 2025s. In finance terms, that’s called discounting.

Once you discount the 2016s and 2019s for the cost of carry, if those adjusted market prices look low, that is not a flaw in the framework. It is simply what the market currently believes those wines should be released at, given that buyers will then have to age them for another nine and six years, respectively.

Which brings us to the central misunderstanding. En Primeur prices are supposed to be low. Buyers pay upfront, take on risk, and wait years before they can drink the wine. Historically, Bordeaux understood this perfectly. As Simon Farr said during the interview for ITMFW, release prices once bore some relation to production costs, adjusted for prestige, while leaving meaningful upside for those willing to store the wines and assume the risk of ageing them. Increasingly, however, some châteaux appear to treat En Primeur as an opportunity to capture the full value of the wine immediately. That misses the point entirely. EP is not about maximising short-term profit but it is about sharing risk between producer, merchant, and buyer.

For collectors, the decision is ultimately quite simple. Buy a 2016 at £100: bottled, aged, proven, and ready. Or buy a young 2025 at £70: unproven and years away from drinking. Is £30 enough to justify the wait and uncertainty? That is the only question that matters within this framework.

Other arguments—provenance, access, relationships—are secondary, as buying from good merchants should offer the same assurances.

If the trade and the châteaux cannot make money at those levels, that is a serious issue — but not one the buyer is obliged to solve.

And buyers should remember that participation in En Primeur is optional. The system only works if it offers a clear advantage: lower prices in exchange for patience. If it does not, there is a very simple alternative — buy back vintages instead and drink them already mature.

None of this denies that wine is a passion asset. People buy bottles for reasons that have nothing to do with economics: birth years, collections, memories, tradition,... Those are all perfectly valid reasons to buy wine. But understanding the economics does not diminish the pleasure. It simply ensures that the decision is made knowingly.

So far, on a comparative basis against previous vintages already trading in the market, only three releases appear genuinely attractive: l’Evangile, Lafleur, and Cheval Blanc.

Thank you as always for being here!

Sara

Support ITMFW

Consider supporting In the Mood for Wine with a paid subscription, or share this with someone who is tired of the usual industry lines such as “Lafite has been released at a 30% discount to last year”

Does cost of carry just involve inflation, or also lost opportunity cost if you’d invested this sensibly in an inflation-busting way, compounded? Wine is a terrible investment at the moment.