What LVMH sales results tell us about the state of the fine wine market

It's a buyer's market

In the mood for wine is the only weekly newsletter for the next-gen of fine wine lovers and investors. It’s free. The best way to keep it free is to share it with everyone. Literally everyone.

Hello fine wine lovers,

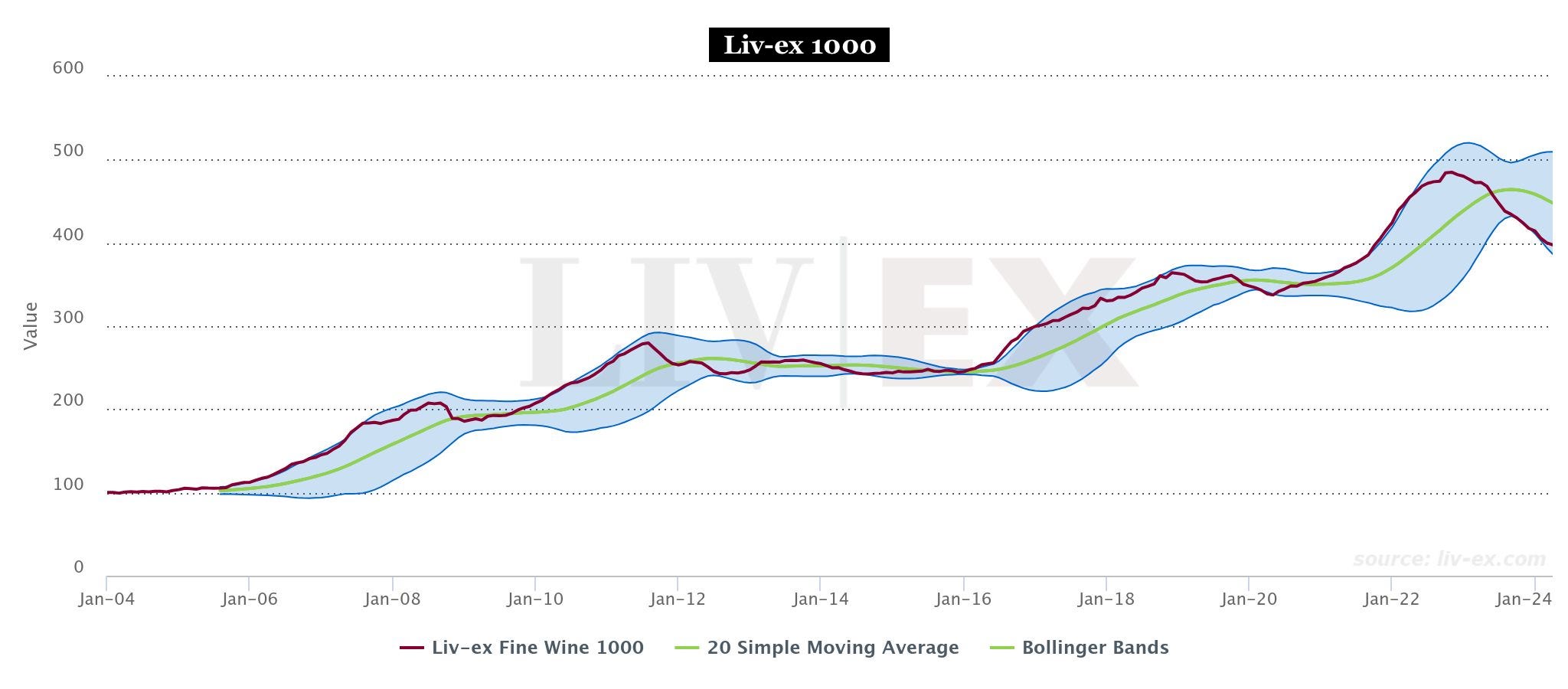

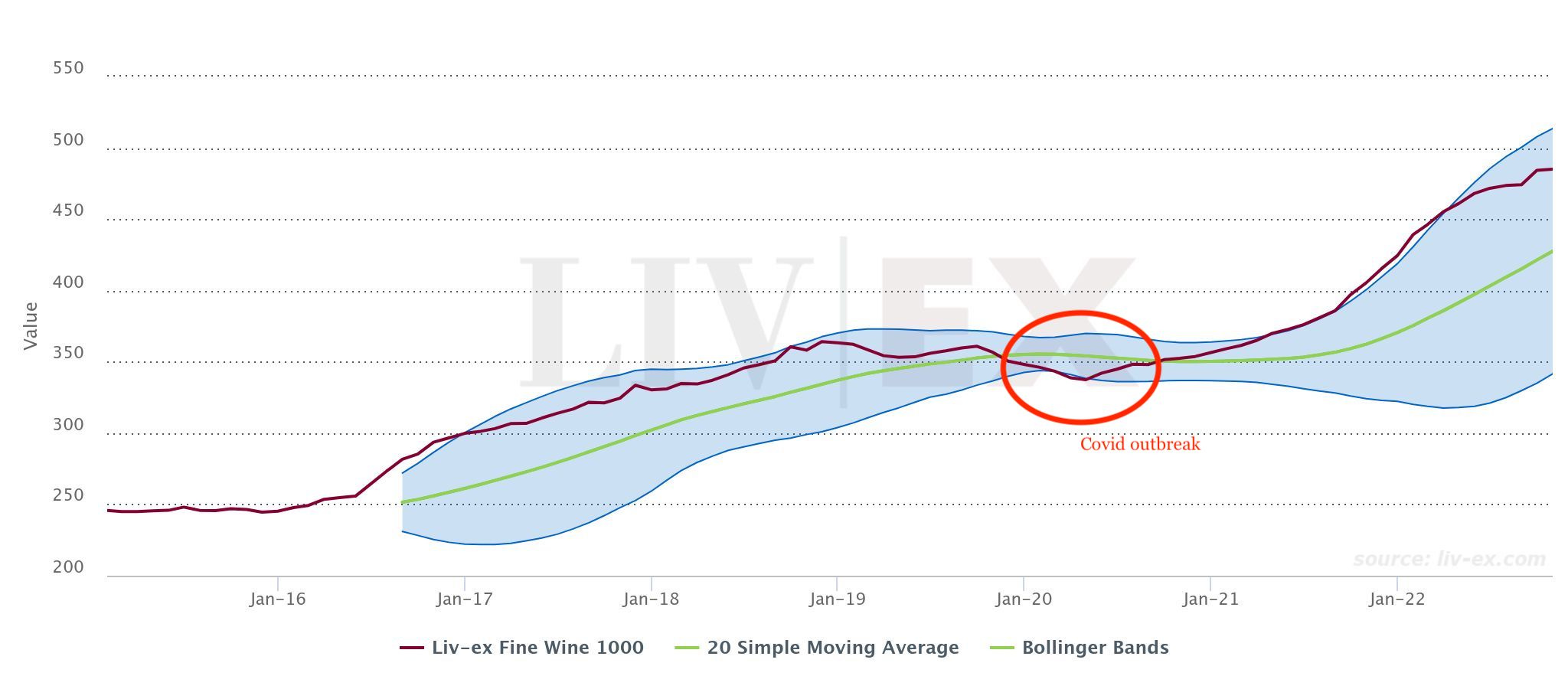

The fine wine market has slipped quietly yet distinctly in its recent performance. The Liv-ex 1000, which includes 1000 of the top names in the space, finds itself navigating through a -4.1% current in this year of 2024, drifting -18% away from the peak it set in October 2022. That is 2 standard deviations away from its average, and since approximately 95% of the values are expected to lie within two standard deviations of the mean in a normal distribution, in plain English, it means that it has moved to a value that is relatively rare and indicates a lower-than-average performance.

This kind of weakness isn’t like any recent crisis in the market before: sharper than 2008 and more prolonged than both 2011 and 2020.

Many are the questions that arise from this. Why now? And what’s causing it? And, more importantly, why is it persisting?

With the Bordeaux En Primeur season upon us, taking the market's pulse is not just wise; it's critical. Let’s look at this from the point of view of the world’s largest luxury conglomerate: LVMH Moët Hennessy. Their Wine & Spirits division accounts for ca. 8% of the business’s total revenues and owns 26 among the best well-known wine & spirits brands in the world.

France:

Dom Pérignon — Champagne

Krug — Champagne

Ruinart — Champagne

Moët & Chandon — Champagne

Veuve Clicquot — Champagne

Mercier — Champagne

Château Cheval Blanc — Bordeaux, Saint-Émilion

Château d'Yquem — Bordeaux, Sauternes

Domaine des Lambrays — Burgundy, Morey-Saint-Denis in the Côte de Nuits

Château Galoupet — Côte de Provence

Château Minuty — Côte de Provence

United States:

Newton Vineyard — Napa Valley, California

Joseph Phelps — Napa Valley, California

Colgin Cellars — Napa Valley, California

Argentina:

Terrazas de Los Andes — Mendoza, Argentina

Cheval Des Andes — Mendoza, Argentina

Spain:

Bodega Numanthia — Valdefinjas, Castile and León

China:

Ao Yun — Yunnan, China

New Zealand:

Cloudy Bay — New Zealand

Other:

Chandon — Argentina, California, Brazil, Australia, China & India

Spirits:

Hennessy — Cognac

Glenmorangie — Scotch Whisky

Ardbeg — Scotch Whisky

Woodinville — American Whiskey

Belvedere — Polish Vodka

Volcan de mi Tierra — Mexican Tequila

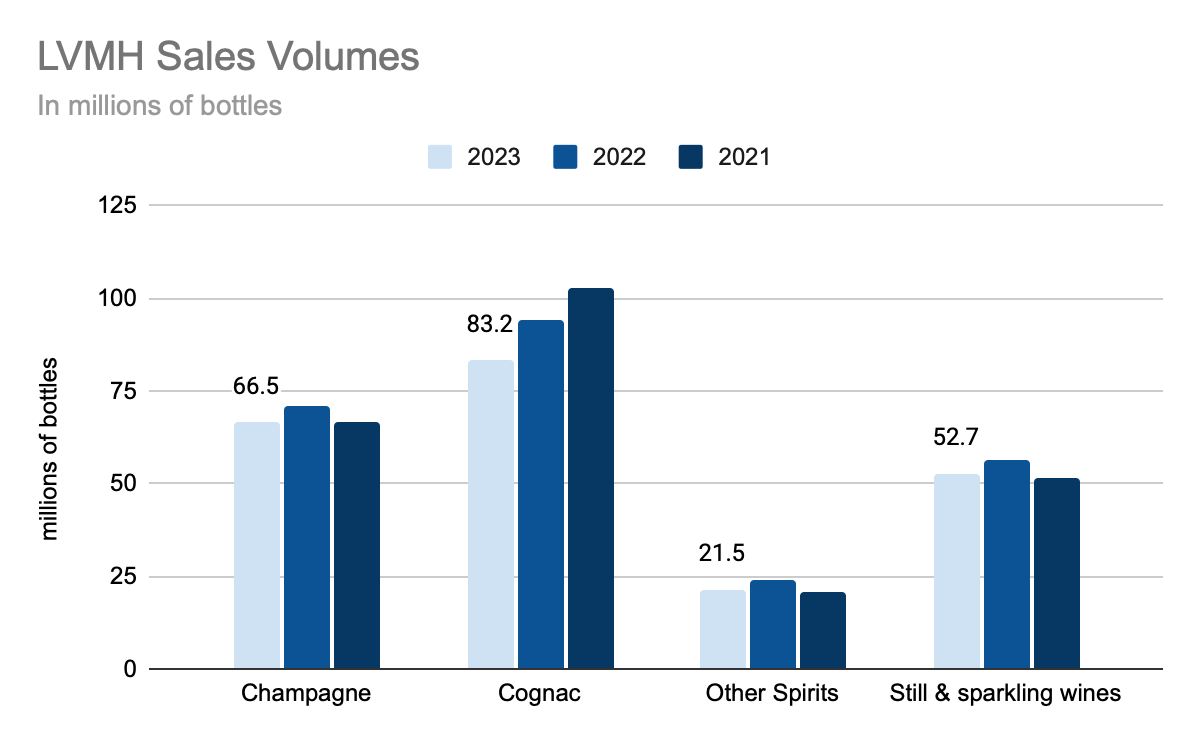

Eminente — Cuban RumTo put into context the impact that LVMH Moët Hennessy has on the wine market, consider the champagne sales. LVMH Moët Hennessy 2023 figures report 66.5 million bottles sold, which is a staggering 22% slice of the entire Champagne market pie, with 299 million bottles sold in total according to CIVC data. That’s almost one in every four bottles. Hence, it's reasonable to say that LVMH Moët Hennessy serves as a telling gauge of the currents and undercurrents within the wine market's broader landscape.

(Also, I really wanted to try this new Substack feature …)

Revenues & Top Line Growth

The Wines & Spirits business group delivered €1.4 billion in revenue for the first three months of 2024. While the total number isn’t relevant for the broader market, it represented a decline of 12% organic revenues in the first quarter of 2024 (compared to their 2023 figure).

Specifically referring to champagne & wine, there was an 8% decrease in demand and a 15% decrease on a reported basis after taking into account a positive 1% structure impact (from the newest acquisition of Château Minuty in Provence) and a negative 8% currency impact from the exposure to the Argentinian peso.

Note that the above-average currency impact reflects the devaluation of Argentina’s pesos to which LVMH have a small exposure through Terrazas de Los Andes and Cheval Des Andes.

In terms of channels, the off-trade segment (supermarkets, merchants, etc.) is doing much worse than the on-trade (bars, restaurants, etc). “The on-trade is not fabulous, don’t get me wrong,” adds Jean-Jacques Guyony, CFO of LVMH Moët Hennessy, “but the off-trade is doing much worse. And conversely, we see that duty-free business in Asia is picking up quite significantly. So, that’s the situation globally: we’re hopeful in the US and wait and see as far as China is concerned.”

The decline in demand during the first quarter 2024 revenues, was driven by a significant destocking. That was a very specific situation because there were high levels of inventories of it in 2023, but “we were a little bit surprised that there was further destocking, and therefore, the sell-in (quantity of goods that a manufacturer sells to a retailer or distributor) was not as good as the sell-out (quantity of goods sold by retailers to the end consumers),” says Jean-Jacques Guiony, CFO of LVMH Moët Hennessy.

This means, quite significantly, that consumer demand wasn’t quite as weak as retailers demand, the weak link being merchants’ cash flows.

Profit Margins

The Wines & Spirit division was able to maintain cost control, especially in marketing expenses due to lower demand in certain countries, namely Asia ex-Japan, with a particular note on weak demand from China and the US.

An analyst on the call asked about some of their wines being discounted, to which the CFO categorically replied that there were no discounts made, “discounts is what Pernod and Rémy do”. But rather a decision to cancel price increases: “we decided to cancel the price increase, and therefore, there was no impact on the profit margin, because it was a price increase that didn't occur, not the same as a discount.”

During the call, there wasn’t a specific mention of which new products. However, in the first quarter of the year, the launch of Château d’Yquem 2021 vintage was indeed kept at last vintage’s prices (£3,180/12x750ml).

Final Notes on the State of the Fine Wine Market

What emerges from LVMH Moët Hennessy results is the stark reality for the wine industry and a significant downturn:

demand decreased ~10% year-on-year;

the decrease in demand have been particularly felt in the form of a weak Chinese New Year and from generally the US;

wine merchants and supermarkets have been the most affected by this decrease in demand;

and, because of that and already previously high levels of stock, the industry have been drastically destocking;

tight cost controls were adopted, especially on the marketing spend in key markets;

and lastly, price increases were cancelled.

Remember when last year, we were pondering whether a 21% increase in Cheval Blanc’s En Primeur price was fairly priced? Well, it seems like the invisible hand of the fine wine market has spoken: it was overpriced.

Pessimism in the air — both the US & China, two of the largest market for fine wines show weakness, not so much as the consumer but the middle men — the merchants, that have been the one squeezed out in this premiumisation inflationary bubble.

Today marks the start of Bordeaux En Primeur season.

With demand down and destocking happening fast, one question stands out: What price drop would bring consumers back? It's a crucial moment for the industry, where the right move could mean a comeback or more tough times ahead.

Thank you again for being part of this community of wine lovers!

This newsletter is free for all readers and the best way to keep it free is to subscribe, re-share it with your wine-lover friends, and follow me on Instagram.

👋 Sara Danese

Comments, questions, tips? Send me a note

Here’s a reading list of some of the most liked content in this newsletter:

One for the cellar — Sassicaia & other Bolgheri 2021 vintage successes.

Cash-Equivalent Wines — a.k.a. a list of the best drinkable fine wines compiled by the best people in the wine trade.

A Tuscan Estate to Watch, Tenuta Sette Cieli, and why I believe this tiny Bolgheri Estate will prove a great investment.

Investment Ideas for Barolo 2019. It does what it says on the tin.

Has Fine Wine Hit Rock Bottom? ChatGPT was a fine wine investment analyst for the day, and shared which corners of the fine wine market are undervalued.

The Ministry of Silly Pricing. Discussing a few interesting releases on La Place …

How's the Champagne market looking? (Jul 2023 update) A collaboration withTom Hewsonlooking at 2013, 2014 and 2015 vintages.

The Earliest Harvest Ever. Talking about Bordeaux EP 2022.

My Fair Value a.k.a. Is Cheval Blanc Undervalued? Again, talking about Bordeaux EP 2022.

Hunting for Barolo 2019 bargains. Looking at the Ravera Cru for Barolo 2019.

Building a 36-bottle cellar, with ChatGPT. A starter cellar. (ChatGPT wasn’t a very great deal of help here.)

The Price of Wine. An economic paper on what are the drivers of fine wine prices in the long run.

Here's the link to the google sheet with the charts in this post: https://docs.google.com/spreadsheets/d/1UuiQmogZKQxV9MZAa5LbmPIOtBFZfioHFhdsQCol6BI/edit?usp=sharing

Another superb piece Sara and always admire the level of detail you go into. I’m in Bordeaux right now - it’ll be interesting to see the result of your poll (which I anticipate many of the Chateaux won’t wanna see!)